India is about to witness the largest private wealth transfer in its history. By 2035, an estimated rupees50 lakh crore will move from one generation to the next. Most of it will be lost, diluted, or disputed, not because of markets, but because of silence.

The entrepreneurs who built India’s post-liberalisation economy are now between 62 and 78 years old. A 2024 survey by a leading Indian private bank found that among households with a net worth above rupees 25 crore, fewer than one in ten had a succession plan their primary inheritors were aware of. The number falls further when accounting for digital assets, overseas holdings, and insurance policies that postdate the original planning, categories that simply did not exist in the vocabulary of the first-generation wealth builder. This piece examines how large the problem is, why it happens, and exactly what a complete plan looks like

1. The numbers behind India’srupees50 lakh crore exposure

2. The five failure modes that repeat across every HNI family

3. From 1991 to the decisive transfer window of 2025–2035

4. What a complete plan looks like, and where most families stop

5. The three legal positions compared for speed, privacy, and protectio

1. The Scale of the Problem

Seventy per cent of Indian family businesses do not survive into the second generation, not just because the underlying business failed, but also because the transfer was unstructured, disputed, or legally frozen. Only 7% of Indian HNIs have a documented succession plan.

The remaining 93% hold wealth across mutual funds, real estate, unlisted equity, insurance, and physical assets with no coordinated plan for what happens when the primary wealth holder is gone. An estimated rupees 35,000 crore already sits as unclaimed assets with Indian financial institutions, the legacy of families who never documented what they owned or who should receive it.

2. Five Ways Wealth Transfers Go Wrong

Succession failures are rarely random. They follow five predictable patterns across Indian HNI families regardless of estate size or geography. The most common is an outdated Will, one that predates significant assets like startup equity, ESOP tranches, or commercial real estate acquired after 2010.

The NRI heir problem is the second most disruptive: when beneficiaries span two tax jurisdictions, settlement timelines stretch to 3–7 years and cross-border tax exposure can consume 15–25% of the value being transferred.

The conflation of personal and business balance sheets adds another layer, founders who live in company flats, hold personal loans on company books, and have never separated their personal net worth from their firm’s can leave estates that take more in legal fees to untangle than a structured plan would have cost. Nomination failures compound everything: rupees35,000 crore in unclaimed assets sits with Indian financial institutions precisely because mutual fund folios, demat accounts, and insurance policies carried no nominee, or the wrong one.

And finally, no one in the family knows where everything is. The average HNI estate misses 12 to 18% of its total value simply because assets were never documented.

3. How We Got Here

The roots of India’s succession crisis run directly back to 1991. The entrepreneurs who capitalised on liberalisation built businesses in an era when estate planning was neither culturally practised nor professionally available to anyone outside the ultra-wealthy. By the 2000s, wealth had compounded across real estate, listed equities, and a newly minted IT-driven HNI class, but succession structures remained absent.

The decade of 2010 to 2020 saw the emergence of India’s 300+ single-family offices, which brought institutional-grade succession planning to the top 0.1% of wealth holders. The vast middle, families with rupees 5 torupees100 crore in assets, was left structurally unserved. That population is now in the decisive window: the founders are in their late 60s and 70s, and the transfer is already under way through gifts, business handovers, and deaths that nobody planned for.

4. The Eight-Point Succession Checklist

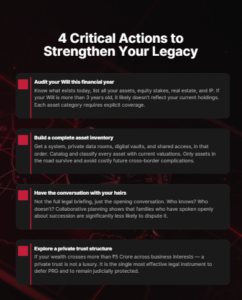

A complete succession plan is not just a Will. It is eight interlocking components that together ensure wealth transfers cleanly, quickly, and to the right people. An updated Will is the foundation, but it must be paired with correctly assigned nominees across every financial instrument, a written asset inventory shared with at least one trusted person, and a legally clean separation of personal and business finances. For families with NRI heirs, a separate cross-border tax and legal plan is non-negotiable, the Foreign Exchange Management Act, double taxation agreements, and US estate tax law each create distinct liabilities that must be addressed in advance. For illiquid assets, real estate, unlisted shares, business interests, a private trust structure dramatically reduces transfer friction and protects against creditor claims. The final component is professional review: a succession plan that has never been examined by a qualified wealth adviser, estate lawyer, and tax professional is a draft, not a plan. The graphic below shows where most Indian HNI families stand today: one of eight boxes ticked.

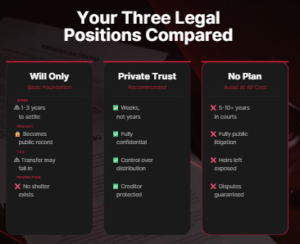

5. Will vs Trust vs No Plan

The Indian Trusts Act of 1882, unchanged in its fundamentals, governs private trust creation in India, yet private trusts remain dramatically underused among HNIs. Budget 2025 introduced crucial clarifications on the taxation of irrevocable trusts, and SEBI’s updated PMS and AIF regulations now permit trust vehicles to access a broader range of structured investment products. A properly constituted private trust bypasses probate entirely, maintains complete privacy, protects assets from creditor claims, and can be structured to optimise tax liability across generations.

By contrast, a Will alone subjects the estate to probate, a process that in Indian courts can take one to three years in an uncontested case and significantly longer when disputes arise. A Will is also a public document once probated, exposing the full estate picture to scrutiny. The worst outcome, dying intestate, triggers the Hindu Succession Act, which applies a fixed formula that rarely matches the deceased’s intentions and virtually guarantees the prolonged family conflict that destroys both relationships and wealth.

What This Means for You

The families that navigate India’s succession crisis well will not be the wealthiest. They will be the ones that started the conversation earliest, with the right advisers, the right legal structures, and a clear-eyed understanding that wealth built across a generation can unravel in a year without a plan to protect it.

Once a founder is medically or legally incapacitated, the planning instruments available become crisis tools, not stewardship tools. The cost of inaction compounds every year it is deferred.

Disclaimer

This content is for informational and educational purposes only and does not constitute investment, legal, or tax advice.

Please consult qualified professionals before making any financial decisions. MintWit Financial Services LLP is an AMFI-registered Mutual Fund Distributor (ARN-283168); however, all investments are subject to market risks and returns are not assured.