Global capital is building Indian healthcare at record speed. Beds are multiplying. Valuations are soaring. But for the patient staring at a Rs 28,000 MRI bill, something doesn’t add up.

A friend walks into a private hospital for a routine knee scan. Thirty minutes, one MRI, and one “quick consultation” later, Rs 28,000 has left his account. The knee was not the only thing hurting. Ask any Indian family and you’ll get the same story in a different font: corporate hospitals feel unaffordable, bills contain mystery tests, and every department seems to want a piece of you.

Now zoom out. KKR holds a stake in Max Healthcare. Blackstone controls Care Hospitals. Temasek has backed multiple healthcare platforms. Bain Capital is in advanced talks to acquire Integrace Health, a speciality pharma and women’s health player, for around Rs 1,200 crore. And the top 13 listed hospital chains are planning to add 14,500 new beds by FY27, backed by a Rs 32,000 crore capex push.

Something large is happening to Indian healthcare. This report maps what it is, who is driving it, and what it means for you, as a patient, as a citizen, and as an investor.

1. The Demand Gap, 1.6 beds, 1.4 billion people

2. The Money Trail, Why global PE won’t stop betting on Indian hospitals

3. The Billing Machine, How hospitals optimise for revenue, not recovery

4. The Building Boom, Who is expanding, how fast, and at what cost

5. The Alternative, A 50-bed model that rewrites the rules

1. The Demand Gap: 1.6 Beds, 1.4 Billion People

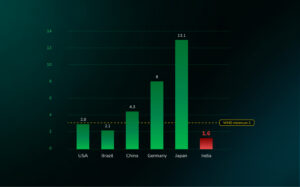

Think of a railway station built for 10,000 people. Now imagine 40,000 arrive every morning. That is India’s hospital system. The country has roughly 1.6 hospital beds per 1,000 people, barely half the WHO’s recommended minimum of 3 per 1,000. The consequences are measurable and painful.

India’s GDP per capita nearly doubled between FY16 and FY25, from $1,774 to $3,374. Yet healthcare spending has barely budged. We spend just 3.8% of GDP on health, compared to the US at over 16%. Worse, most of that gap is filled not by the government but by individuals. Indians pay 63% of their medical expenses out of pocket, one of the highest rates among comparable economies.

The burden is not just financial, it is civilisational. According to data from Brookings India and NITI Aayog, 7% of India’s population is pushed into poverty every single year due to healthcare expenses. The government’s flagship scheme Ayushman Bharat PMJAY relies on the private sector for 52% of its hospitalizations and 66% of its total expenditure, even though private hospitals make up only 45% of empanelled facilities.

2. The Demand Gap: 1.6 Beds, 1.4 Billion People

Private equity’s logic in healthcare is not complicated, it’s structural. Healthcare demand doesn’t contract during slowdowns. People don’t defer cancer treatment because the market is down. That makes it one of the most recession-resistant sectors on earth.

India adds a second layer of appeal: scale. The Indian healthcare market is already estimated at over $370 billion, and it is growing faster than the economy. The explosion of lifestyle diseases, obesity, diabetes, cardiovascular disease, and the rapid expansion of health insurance coverage all point in the same direction: more patients, more procedures, more revenue, for longer.

The names investing in this thesis are not small. KKR built exposure through Max Healthcare. Blackstone controls Care Hospitals. Temasek has backed multiple platforms. The latest signal is Bain Capital’s reported Rs 1,200 crore move on Integrace Health. For private equity, the playbook is clear: acquire, consolidate, expand geographically, improve EBITDA margins, and exit at a premium multiple. What looks like routine deal activity is actually something larger, global capital isn’t just participating in Indian healthcare, it’s building it.

3. The Billing Machine: How Hospitals Optimise for Revenue, Not Recovery

Here is a paradox worth sitting with: MRI machines, surgical robots, and diagnostic equipment have all become 40% cheaper over the last decade. Yet hospital bills have risen by nearly 300% over the same period. Equipment got cheaper. Care got more expensive. Something in between is extracting value, and it isn’t the patient.

The structure of hospital economics creates a powerful set of incentives that point away from the patient. A routine consultation earns a hospital roughly Rs 500. A surgery earns Rs 5 lakh. A normal delivery brings in Rs 30,000. A C-section brings Rs 1 lakh. The National Family Health Survey found that in states like Telangana, private hospitals perform C-sections in over 60% of births, four to six times the WHO’s recommended rate of 10-15%.

Doctors are not villains in this story. They are professionals operating inside a system that rewards intervention over prevention, procedures over patience. More diagnostics, longer stays, more referrals, these generate departmental performance scores. The incentive structure does not ask whether the test was necessary. It only asks whether the test was billed.

4. Building Boom: Who Is Expanding, How Fast, and at What Cost

For years, India’s corporate hospital sector grew by charging more per occupied bed rather than building more beds. Now, for the first time in over a decade, that calculus has changed. The sector is entering its biggest expansion phase since the mid-2000s.

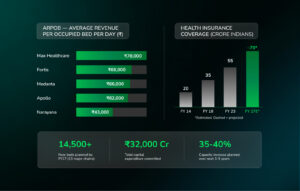

A group of 13 hospital chains are expected to add approximately 14,500 new beds by FY27, a 26% capacity addition, requiring capex of roughly Rs 32,000 crore. The broader ambition is even larger: 35–40% capacity increase over the next three to five years. Health insurance coverage has jumped from about 20 crore Indians in FY14 to nearly 55 crore by FY23.

The market leaders, Apollo, Max, Fortis, Medanta, Narayana, have grown revenues at a 14–22% CAGR over the last three years. Their ARPOB numbers are striking: Max earns Rs 78,000 per occupied bed per day, Fortis Rs 68,000, Medanta Rs 66,000, Apollo Rs 62,000. These numbers explain why these chains trade at 25–50x EV/EBITDA. Investors aren’t just buying healthcare growth, they’re paying up for pricing power that smaller hospitals simply cannot replicate.

5. The Alternative: A 50-Bed Model That Rewrites the Rules

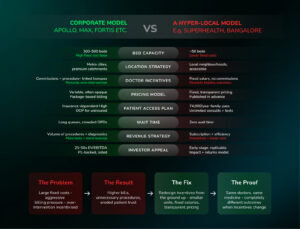

The assumption baked into everything above is that hospitals have to be built this way, large, capital-intensive, metro-focused, procedure-optimised. But a small number of operators are demonstrating that the problem was never the medicine. It was the business model underneath it.

Consider the contrast with a hyper-local model like the one operated by Superhealth in Bangalore. Instead of a 300–500-bed flagship hospital that needs years of aggressive billing just to service its fixed cost base, the model deploys 50-bed facilities in local neighbourhoods. The math changes completely. Overheads are lower, so the pressure to bill aggressively is structurally reduced.

No commissions. No performance bonuses tied to procedures or surgeries. Fixed, transparent pricing. Unlimited consultations under a family plan priced at Rs 4,000 a year for a family of four, with all tests and scans covered. The model eliminates the financial reward for over-intervention. The lesson: private healthcare can be built differently. The current dominant model has been engineered for revenue optimisation, not patient outcomes. That is a design choice. And design choices can be remade.

What This Means for You

Here is the uncomfortable truth about Indian healthcare right now: the people who understand how this system is being built are the same people positioned to benefit from it. And the people who don’t, keep paying for it, in both senses of the word.

The supply gap is real and the demand is structural. Insurance penetration is still sub-50%. India’s population is ageing. Lifestyle disease burden is climbing. Medical tourism is scaling. None of these forces reverse in a downturn. The top hospital chains, Apollo, Max, Fortis, Medanta, Narayana, are not just growing; they are compounding, with pricing power, geographic expansion headroom, and improving ROCE. At 25–50x EV/EBITDA they are not cheap. But the question worth asking isn’t whether they’re expensive, it’s whether the runway justifies the multiple. For most of these names, the answer has consistently been yes.

The more interesting play, arguably, is one step removed. The diagnostics chains, the medical device distributors, the hospital-grade real estate operators, the health insurance platforms, these are the picks-and-shovels of a Rs 32,000 crore capex cycle. Less discussed, less crowded, and with structurally similar tailwinds.

But here is what separates the informed observer from the passive one: the PE playbook in Indian healthcare is not just about financial returns. KKR, Blackstone, Temasek, they are not building charitable infrastructure. They are building assets they intend to own, scale, and exit at a premium. When that cycle plays out, through IPOs, strategic sales, or secondary deals, the returns will accrue to those who entered early and understood the thesis deeply. That window is still open. It will not stay open forever.

One last thing. Every person reading this will, at some point, sit across a doctor in a private hospital and be handed a bill they don’t fully understand. When that moment comes, and it will, knowing that the system around you is optimised for revenue rather than recovery isn’t cynicism. It is the most practical form of intelligence you can carry into that room. Ask questions. Request itemised bills. Compare. The information asymmetry in Indian healthcare is vast, but it is not insurmountable, and the people who close it, even partially, consistently come out better on the other side.

The next five years will determine who this boom ultimately serves. Be the kind of person it serves.

Disclaimer:

This content is for informational and educational purposes only and does not constitute investment, legal, or tax advice. Please consult qualified professionals before making any financial decisions. MintWit Financial Services LLP is an AMFI-registered Mutual Fund Distributor (ARN-283168); registration does not assure returns.