Seventy-five billion dollars. A 1.75 trillion dollar valuation. One man holding 83.8% of the votes. Here is what an Indian investor needs to know.

On June 12, 2026, SpaceX will list on the Nasdaq stock exchange. The ticker symbol is SPCX. The deal will be the biggest IPO ever recorded, anywhere in the world.

The previous record was Saudi Aramco at 29 billion dollars in 2019. SpaceX wants 75 billion. That is two and a half times bigger. In one morning.

The total value of the company at listing? 1.75 trillion dollars. In rupees, roughly 146 lakh crore. That is bigger than every Indian IPO of the last five years combined, multiplied many times over.

Most Indian investors have not really followed SpaceX. The name is familiar. Elon Musk is famous. But what does the company actually do? Why is it worth this much? And what happens if you, sitting in India, want to buy a share?

- The Business- three companies hiding inside one rocket

- The Man- why this is really Musk’s IPO

- The Price- is 1.75 trillion dollars fair?

- The Terms- what Musk has demanded from shareholders and banks

- The Risks- what could go wrong

- What’s In It For You- the Indian investor’s playbook

1. Three companies hiding inside one rocket

SpaceX started in 2002 in a small office in California. By 2008, the company was almost out of money. Three rockets had failed in a row. They could afford one more attempt.

The fourth rocket reached orbit. SpaceX survived.

The real breakthrough came seven years later. On December 21, 2015, a Falcon 9 rocket went to space and came back to land on its own legs. No country had ever done this. A rocket that returns can be used again, like a flight or a car.

This one change cut the cost of going to space by 30 times. In the 1990s, sending 1 kg of cargo to space cost 50,000 dollars. Today, SpaceX does it for 1,500.

That single number is the whole story. Cheap rockets opened up everything. And SpaceX used those cheap rockets to build three different businesses.

Launch. Falcon 9 and Starship rockets. The customers are NASA, the US military, and private companies sending satellites to space. SpaceX today launches the majority of everything that goes into orbit, globally.

Starlink. A satellite internet service. Picture a small dish on your roof, like a Tata Sky dish, but instead of TV you get fast internet anywhere on earth. Even in villages with no cable. There are 11,000 Starlink satellites in orbit and nearly 10 million people pay every month.

xAI. The AI company that makes Grok, a chatbot similar to ChatGPT. SpaceX bought xAI in February 2026 in an all-stock deal.

Three businesses inside one company. Revenue went from zero in 2008, to 15 billion dollars in 2025. The first profit came in 2023.

2. Why this is really Musk’s IPO

Elon Musk owns about 42% of SpaceX. He also runs Tesla, owns X (the company formerly called Twitter), runs Neuralink, and started The Boring Company. He is already the richest person who has ever lived. After the SpaceX IPO, he could become the world’s first trillionaire.

The math is straightforward. His SpaceX stake at a 1.75 trillion dollar valuation would be worth about 735 billion. His Tesla stake is worth another 180 to 200 billion. His X holding adds more. In November 2025, Tesla shareholders also approved a new pay package that could give him up to 1 trillion dollars more if Tesla hits certain growth milestones over ten years.

Add it up and his total wealth crosses 1 trillion dollars within months of the SpaceX listing. No human being has ever held this much money. That alone makes the IPO historic.

But Musk did not build SpaceX for money. From day one, he has said the goal is to make humans a “multi-planetary species.” In plain words: send people to Mars and start a colony there.

This sounds like science fiction. Musk treats it as a project plan. Starship, the next-generation rocket SpaceX is building, exists specifically to carry humans to Mars. Musk’s public timeline is unmanned missions to Mars by 2028, and humans by 2030. Parts of his Tesla compensation package are actually tied to Mars colonisation milestones.

Most investors do not believe these dates. But many of them buy the stock anyway, because Musk has a habit of delivering things others called impossible. Reusable rockets. Mass-market electric cars. Brain implants that work. He misses deadlines, but he ships the product.

This is what you are buying when you buy SpaceX. Not just a company. A bet on one man continuing to do unreasonable things for the next 20 years.

3. Is 1.75 trillion dollars fair?

The simplest way to judge an IPO price is to compare the company’s value to its yearly revenue. This is called the price-to-sales ratio. Higher number means a richer price.

Microsoft listed in 1986 at 2.5 times revenue. Conservative.

Google listed in 2004 at 7 times. Fair.

Alibaba listed in 2014 at 20 times. Worked out fine.

Facebook listed in 2012 at 28 times. People called it crazy at the time. The price worked out because Facebook grew fast enough.

SpaceX wants 115 times.

That is unprecedented for a company of this size. The only way this price makes sense is if SpaceX grows roughly 10 times over the next 5 to 7 years.

The bulls say yes, it can. Starlink keeps adding millions of subscribers every year. Starship will open up new businesses like space tourism, moon cargo, and even data centres in orbit. The xAI deal adds an AI angle. SpaceX is the only company in the world that owns rockets, satellites, AI chips, and AI software all under one roof.

The bears point out that Nvidia, the hottest AI company on earth, trades at only 25 times revenue. Apple trades at 9 times. SpaceX is being priced at four times Nvidia’s multiple while making one-tenth of its revenue. The price assumes everything goes right for ten years. In practice, things rarely do.

4. What Musk has demanded from shareholders and banks

Most IPOs are designed to please new shareholders. SpaceX’s IPO is designed to please Elon Musk. He has put three sets of conditions on this deal.

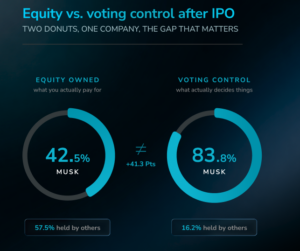

Demand 1: He keeps the votes. SpaceX has set up two classes of shares. The Class A shares the public can buy carry 1 vote each. The Class B shares Musk holds carry 10 votes each. After the IPO, Musk will own 42% of the equity but 83.8% of the voting power.

In plain words: even if every other shareholder voted against him on something, Musk still wins. He cannot be removed as CEO. He cannot be removed from the board. The only person who can fire Musk from SpaceX is Musk.

Demand 2: No court access. Shareholder disputes go to private arbitration, not the courts. SpaceX is also incorporated in Texas, where a special rule says you need to own at least 1 million dollars worth of stock, or 3% of the company, just to propose a shareholder vote. For an Indian retail investor, getting heard is essentially impossible.

Demand 3: Conditions on the bankers themselves. SpaceX hired 21 banks to handle the IPO. Goldman Sachs leads. Morgan Stanley sits second. JPMorgan, Bank of America, and Citigroup follow. But Musk made unusual demands of them. Reports say:

- All deal documents had to be reviewed using Grok, his own AI tool. Not ChatGPT.

- The main banker meetings happened at Starbase in Texas, SpaceX’s rocket facility, not at Wall Street offices.

- Musk personally vetted every senior banker who worked on the deal.

- Fees were squeezed to roughly 1%, half the normal rate for a deal this size.

The banks accepted these terms because the deal is too big to walk away from. CalPERS, the largest US pension fund, has formally objected to the voting structure. SpaceX has not responded.

5. What could go wrong

Five risks worth understanding before you buy.

One risk deserves a little more attention. Day-one supply. In most IPOs, insiders are not allowed to sell their shares for six months after listing. This is called the lock-up period. SpaceX has reportedly waived this. Early employees, original investors, and even Musk’s own holding can be sold from the very first day of trading.

What this means for you: if you buy SPCX on day one, you may be buying from someone who has been holding the stock for 15 years and knows the company inside-out. They get cash. You get exposure. Historically, this kind of structure produces a sharp price pop on day one followed by months of slow decline as insider selling absorbs retail demand.

Disclaimer:

This content is for informational and educational purposes only and does not constitute investment, legal, or tax advice. Please consult qualified professionals before making any financial decisions. MintWit Financial Services LLP is an AMFI-registered Mutual Fund Distributor (ARN-283168); registration does not assure returns.