Picture a country where the smartest thing you could do with your money was nothing at all. Where leaving it in the bank, earning almost no interest, quietly beat almost every other option. Not for a year or two, but for an entire generation. That country is Japan. For three decades it lived in a world where money had no price. On 16 June 2026, that world ended. The Bank of Japan lifted its policy rate to 1 percent, the highest since 1995. From Pune that number looks like a rounding error. For Japan, it is the ground shifting. Here is how a nation forgot what interest was, and why its memory coming back reaches all the way to your portfolio.

IN THIS EDITION

- Half the wealth, under the mattress

- The thirty-five-year hangover

- How Japan became the world’s lender of free money

- The week money got a price tag

- Who pays when free money ends

- Half the wealth, under the mattress

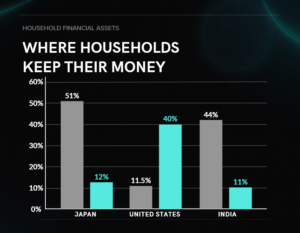

Start with one strange fact. At the end of March 2025, Japanese households were holding more than half of their financial wealth in plain cash and bank deposits. Barely a tenth sat in stocks.

That is the opposite of how the rest of the rich world behaves. In the United States, cash is just over a ninth of household wealth, while more than 40 percent rides in equities. Even Indian households, in a far poorer economy, keep a smaller share of their money idle in deposits than the Japanese do.

This looks irrational until you see the incentive behind it. Almost everywhere, cash slowly rots. Inflation eats its value every year, so sitting still is a way to lose. The only defence is to put money into something that grows faster than prices.

Japan learned the reverse. For thirty years its prices barely moved, and in plenty of years they actually fell. When prices fall, a still pile of cash buys more next year than it does today. Doing nothing was not laziness, it was a winning trade. And a winning trade, repeated long enough, stops being a choice and becomes a reflex.

2. The thirty-five-year hangover

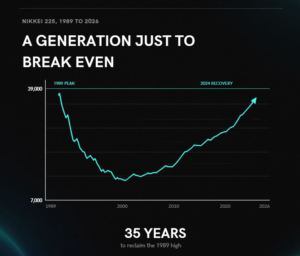

To understand why cash won, rewind to the late 1980s. Japanese stock and land prices had floated free of reality. At the peak, the land under Tokyo’s Imperial Palace was reckoned to be worth more than the entire state of California. Then the bubble burst, and the floor gave way.

The collapse was total. Asset prices cratered, banks drowned in bad loans, and companies simply stopped spending. One number captures the damage. If you had bought the Nikkei at its December 1989 high, you would have waited roughly thirty-five years, until early 2024, merely to get your money back. A whole working life, no gain.

Faced with that, businesses changed their nature. The economist Richard Koo named it a balance sheet recession. Companies stopped chasing growth and spent years doing nothing but paying down debt, refusing to borrow even when loans were practically free. With nobody borrowing or spending, jobs disappeared, wages were cut, and households delayed every purchase they could. Falling prices made waiting rational, and waiting pushed prices down further. The snake ate its own tail, and the loop ran for years.

3. How Japan became the world’s lender of free money

An economy that refused to grow had little use for money at home. Banks could not find anyone worth lending to at a decent return. Insurers could not grow the savings they needed to cover future claims. The one borrower left standing was the government, which loaded up on debt that cost almost nothing. By early 2025 it owed more than two and a half times the size of its entire economy, at an average interest rate under 1 percent.

The more interesting action, though, happened offshore. When money is free in one country and expensive everywhere else, a tidy trade opens up. You borrow yen at near-zero cost, swap it for dollars or rupees, and put it into something that actually pays a return. The difference is yours to keep. This is the famous yen carry trade, and for years it was about as close to free money as global finance offers.

By one assessment it had ballooned past 40 trillion yen, more than 23 lakh crore rupees, by August 2024. And a striking share of it washed onto Indian shores as foreign portfolio money. The table below tracks where yen-funded money actually travelled. India drew about 23 percent of the inflows and saw its yen-funded assets balloon by 251 percent, the steepest jump of any market on the list. Put plainly, cheap money borrowed in Tokyo was quietly helping lift markets in Mumbai.

4. The week money got a price tag

The thaw began in an unlikely place: a war. When Russia invaded Ukraine in 2022, the food and fuel that Japan imports almost entirely became far more expensive overnight. Inflation, a stranger for three decades, walked back through the door.

This time it stuck. With a shrinking, ageing workforce, Japanese workers finally had bargaining power, and in 2024 they won average pay rises of 5.1 percent, the largest in 33 years. Higher wages let firms pass on higher prices, and most importantly, people started to expect prices to keep rising. That expectation is the fuel inflation runs on, and Japan had been missing it for a generation.

So the Bank of Japan began dismantling thirty years of emergency machinery. It scrapped negative rates in March 2024, then climbed in careful steps: 0.25 percent that July, 0.5 in January 2025, 0.75 last December. Then, on 16 June 2026, with a fresh oil shock from the Iran war piling on the pressure, it pushed past 1 percent for the first time since 1995. The vote was near-unanimous, taken with the governor absent in hospital and his deputy in the chair. After three decades, money in Japan had a price tag again.

5. Who pays when free money ends

A rate hike sounds like good news, a sign of health returning. For much of Japan, it is a deeply awkward adjustment.

Take the banks. Higher rates should widen their lending margins, which helps. But the old government bonds sitting on their books, stuffed with tiny coupons near 0.5 percent, look unattractive next to fresh bonds paying real interest. Their market value has fallen, eating into the capital of smaller lenders. Life insurers, long the government’s most reliable buyers, are nursing the same bruise and turning shy of very long-dated debt.

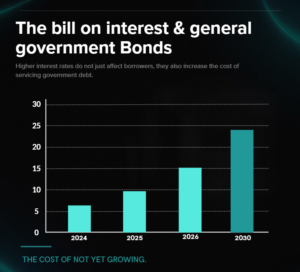

The government feels it most of all. As cheap old bonds mature, it has to roll them over at real rates. Its interest bill on general bonds has climbed from around 8 trillion yen in fiscal 2024 toward 13 trillion in fiscal 2026, and credible projections see it roughly doubling again by 2030. Counting everything, debt servicing already swallows close to a quarter of the national budget.

And the carry trade? As Japanese yields rise, borrowing yen to invest abroad stops being a free lunch. Some of that money is heading home, and that unwind may be one quiet strand in India’s recent foreign-investor outflows. The twist is that Japanese stocks have welcomed all of this. The TOPIX index is up more than 100 percent in five years, because investors read higher rates as proof of real growth and a reason to move out of cash.

Reading the shift from India

If you hold global assets or advise anyone who does, Japan’s shift matters far more than its modest 1 percent suggests.

Free yen funding is fading. The carry trade that helped pad emerging-market inflows, India very much included, is shrinking. A meaningful chunk of the foreign money that lifted Indian equities in recent years was borrowed in Tokyo, and some of it is now being recalled. Expect that to keep adding noise to FPI flows, and don’t mistake every wobble for a verdict on India’s own fundamentals.

The currency map is being redrawn. A firmer yen and real Japanese yields make Japanese assets genuinely competitive for the first time in a generation, which can pull global capital toward Tokyo and away from higher-risk markets. For NRI investors with yen exposure or Japan-linked holdings, this is a real re-rating to reassess, not a passing blip.

The price of money shapes everything. Japan is living proof that interest rates quietly govern how families save, how firms invest, how governments borrow, and where capital chooses to travel. When that price changes, every one of those habits has to be relearned. For Indian investors used to a steady drip of cheap foreign money, it is worth knowing exactly where some of that money came from, and what happens now that its source is no longer free.

The old world is gone.

What replaces it, nobody yet knows.

Disclamer- This content is for informational and educational purposes only and does not constitute investment, legal, or tax advice. Please consult qualified professionals before making any financial decisions. MintWit Financial Services LLP is an AMFI-registered Mutual Fund Distributor (ARN-283168); however, all investments are subject to market risks and returns are not assured.