Why the world’s clean energy revolution is solving one problem by creating three new ones, and where India sits in the middle of it all

The last six months have reshuffled the global energy order in ways nobody fully predicted. Oil prices jumped when the Hormuz crisis hit. EV demand climbed across three continents, Europe, Asia, and parts of the Americas. Japan started framing electrification as a national security issue, not a climate one. And yet, simultaneously, global coal supply investment climbed to its highest level in more than a decade, at around $180 billion. Gas plant orders in the United States hit a 25-year peak, not because of some geopolitical emergency, but because AI data centres need power that the grid simply cannot deliver fast enough.

This edition is about that contradiction. The world is moving toward clean energy, genuinely and at real speed. But the transition is not clean, not equal, and not as independent from old problems as most people assume. It has created new chokepoints, new dependencies, and a funding gap that is quietly widening between the countries that can afford this shift and those that cannot.

And India, as usual, sits right in the uncomfortable middle of it.

1. The Two-Track Bet India Is Running

2. Why “Energy Security” Doesn’t Mean What It Used To

3. The China Problem Nobody Talks About Loudly

4. The Cost of Borrowing Is Quietly Killing Green Ambitions

5. Fossil Fuels Just Got a Second Lease on Life

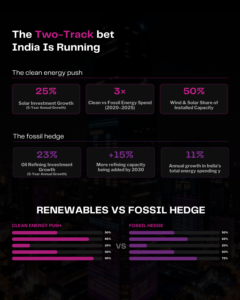

1. The Two-Track Bet India Is Running

India is doing something that looks contradictory on paper.

Over the last five years, we have pushed harder into renewable energy than almost any large economy. Solar investment is growing at roughly 25% a year. Wind and solar now account for more than half of our installed power capacity. For every rupee India spent on fossil-fuelled electricity five years ago, it now puts three times as much into clean power and nuclear. That is not a small shift.

And then, in the same breath, we have been building oil refineries at the fastest pace in years. Refining investments have grown at around 23% annually over the same period. We are on track to add roughly 15% more refining capacity by 2030. All of it processes imported crude.

So why go all-in on energy independence while simultaneously deepening your dependence on imported oil?

It helps to look at what India has actually achieved on the clean side. In 2025, India added over 37 GW of solar capacity, surpassing the United States, which added 34 GW, to become the world’s second-largest solar growth market, behind only China. Our cumulative installed solar capacity crossed 155 GW, helping India fulfil its Paris Agreement commitments ahead of schedule. (Source: IRENA, MNRE 2025)

The answer to the contradiction, then, is not confusion. It is a hedge. India is too large and growing too fast to pick just one direction. Our total energy spending is rising about 11% a year, one of the fastest rates in the world. We need energy urgently and in all its forms. Given our constraints, expensive capital, a complicated relationship with China, and a still-developing grid, we cannot afford to wait for the clean transition to be complete before meeting today’s demand.

This is the energy paradox India is navigating. And as a new report from the International Energy Agency makes clear, we are not alone. The whole world is caught in the same bind, just in different configurations.

2. Why “Energy Security” Doesn’t Mean What It Used To

For most of the last fifty years, energy security meant one thing: keep the fuel flowing. When the 1973 oil shock hit, the world responded by finding oil in safer places, the North Sea, Alaska, and by squeezing more efficiency out of every barrel through fuel economy standards.

That model is being retired.

The Hormuz crisis earlier this year was the latest reminder that fuel-based energy security is inherently fragile. A chokepoint tightens, oil prices spike, and every importing country feels it within days. Japan and Korea, which import nearly all of their fuel, responded by deploying public funds to electrify buildings and heating systems. They sold this to their voters as national security spending, not climate policy. Countries across the EU accelerated EV adoption. Vietnam picked up the pace on clean energy tenders.

The IEA’s position on this is blunt: the most reliable defence against being held hostage by oil is to not need it. Electricity generated domestically from sun and wind cannot be blockaded or priced out by a cartel sitting on the other side of the world. That logic now directs close to 60% of all global energy investment, into generating, transmitting, storing, and running things on electricity.

But the IEA also flags something that is not getting the attention it deserves. Electrification does not end a country’s dependence on the outside world. It only changes what that dependence looks like.

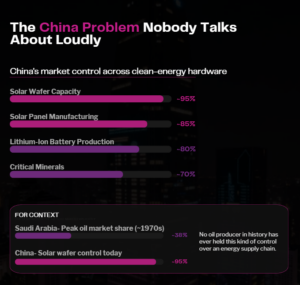

3. The China Problem Nobody Talks About Loudly

An oil-dependent economy keeps buying oil. An electrified one keeps buying something else: hardware.

Solar panels. Batteries. Transformers. Cables. Grid equipment. These are the physical inputs that make a clean power system run. And right now, the supply chain for almost all of them runs through one country.

China manufactures roughly 85% of the world’s solar panels. It produces around 80% of global lithium-ion batteries. Its factories make approximately 95% of the silicon wafers that go inside solar cells. And beyond the equipment itself, China controls more than 70% of the global market for 19 of the 20 minerals that the IEA considers strategically critical for the clean transition.

No oil producer in history has ever held this kind of control over an energy supply chain. Saudi Arabia at its peak was nowhere near this level of dominance.

This puts countries that are trying to decarbonise while also reducing geopolitical risk in a genuinely awkward spot. For India specifically, the tension is explicit. We do not fully trust China as a supplier, but building domestic manufacturing at the required scale takes time and capital that we do not have in abundance right now. So we hedge. We buy Chinese solar panels while also expanding oil refining, so we are not entirely dependent on either transition path.

What the world is effectively doing is trading an oil dependence it spent decades learning to manage for a manufacturing dependence it is only just beginning to understand.

4. The Cost of Borrowing Is Quietly Killing Green Ambitions

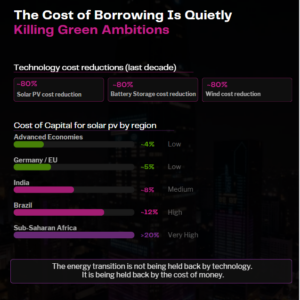

electric vehicles have each fallen in cost by roughly 80%. Without those reductions, the clean energy investments expected in 2026 alone would cost nearly twice as much to deliver the same capacity additions. That is not a marginal improvement. It is the difference between a viable transition and an aspirational one.

But cheaper panels do not help if you cannot borrow money to buy them.

Clean energy infrastructure is front-loaded. Unlike a gas plant, where you spend less upfront and keep paying for fuel over years, a solar or wind farm requires almost all of its investment at the very start. The fuel itself, sun and wind, costs nothing. That makes the cost of the loan the single most consequential variable in the project economics. It determines whether the project gets built at all.

This is where the clean transition reveals its deepest structural inequality.

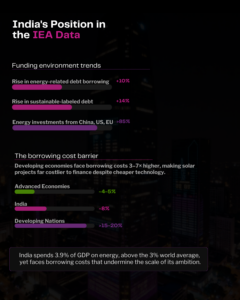

A solar project in Germany or the United States can be financed at rates in the mid-single digits. The same project in India carries a cost of capital closer to 9 to 13%. In South Africa or Brazil, it is similar. In much of Sub-Saharan Africa, it runs above 20%.

India’s own numbers from the IEA data are worth pausing on. Our energy investment per capita sits at $112, against a world average of $396. We are spending 3.9% of GDP on energy investment, compared to 3% globally. We are leaning in harder than most. But we are doing it with expensive money, which means every project we build carries a structural cost disadvantage that quietly erodes the economics from day one.

Here is the number that captures how significant this really is. If borrowing costs in developing economies came down by just a single percentage point, their combined annual savings on clean energy financing would reach approximately $30 billion by 2035. That one statistic tells you more about the real obstacle to the energy transition than any technology headline.

Meanwhile, the funding environment is moving in the wrong direction. Energy-related debt borrowing rose about 10% last year, but equity investment, grants, and subsidies edged down. The market for sustainable-labelled debt shrank by around 14% as lenders returned to judging projects on plain economics rather than green branding. Philanthropic capital, which once backstopped early-stage projects in frontier markets, has thinned considerably.

The capital for clean infrastructure is increasingly sitting with a small group of very large institutions, pension funds, insurers, and asset managers, who now hold over 85% of the largest private energy companies. These institutions are chasing low-risk, predictable returns. That description does not fit most developing economies.

The result is predictable. China, the United States, and the European Union together account for roughly two-thirds of global clean energy investment. The rest of the world shares less than 30%.

5. Fossil Fuels Just Got a Second Lease on Life

At the start of 2025, it genuinely seemed like coal was on its way out as a global energy backbone. Then Hormuz happened, and the calculus shifted.

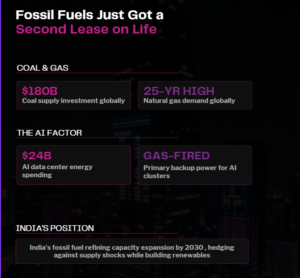

Countries that could not afford clean energy, or did not trust the supply chains behind it, looked at coal and found it oddly reassuring. It is widely available, relatively immune to geopolitical chokepoints, and does not require an IMF loan to access. Global coal supply investment has now climbed to its highest level in more than a decade, at around $180 billion.

Natural gas has surged too, but for a completely different reason. The United States, the world’s richest economy, is ordering gas-fired power plants at the fastest rate in 25 years. This is not capital starvation. It is AI.

Data centres require enormous, continuous, uninterruptible power. AI’s electricity demand is growing faster than clean grids can physically respond to. In just the past year, the US placed approximately $24 billion worth of gas-related orders specifically for data centre projects. If American data centres were their own country, they would rank as the world’s second-largest destination for gas turbines. The AI demand timeline is simply too compressed for solar farms and grid upgrades to fill the gap in time, so gas fills it instead.

There is something almost absurd about this. The same moment pushing the world toward electrification is, for entirely structural reasons, giving fossil fuels a second wave of investment. For India, coal remains a strategic reserve for exactly the same reasons it does for Indonesia or Vietnam, not because we prefer it, but because we cannot afford to be without it while the alternatives scale up.

Conclusion

The clean energy transition is real. The momentum is real. Solar costs have dropped 80% in a decade. Close to 60% of global energy investment now goes into electricity in some form. Countries that built clean capacity over the last ten years are measurably less exposed to oil price shocks today. The IEA estimates over $260 billion in fossil fuel import costs were avoided in 2025 alone, because of clean investments made since 2015.

But the transition is not evenly distributed, and that gap is not closing on its own.

The countries that can afford clean energy cheapest are the ones that needed it least. The hardware supply chain runs through a single country. The capital markets that are supposed to fund the developing world’s transition are retreating toward safe, rich-country assets.

India is neither fully exposed nor fully insulated. We are building green capacity at scale while keeping fossil fuel infrastructure as a hedge. That is not incoherence, it is the only rational response to a moment where the clean path is necessary, expensive, and partially blocked. We have to guard against two risks at once: being shut out of the clean future, and being caught short in the fossil-based present.

Energy as a long-term asset class is changing. Clean energy infrastructure is now predominantly institutional, dominated by large pension funds and asset managers. Retail exposure is mostly through equity, which carries a different and often underappreciated volatility profile.

India’s refinery build-out is not backward thinking. It is a deliberate supply-side strategy. Companies in the refining and petrochemicals space may carry more tailwind than the energy-transition narrative gives them credit for.

Capital cost risk is real and underpriced. Any investment thesis around renewable project developers in emerging markets needs to factor in the cost of capital, not just the technology economics. The two are not the same calculation.

The China hardware question is unresolved. India’s PLI scheme and PM KUSUM for domestic solar manufacturing are direct policy bets with supply chain investment implications across the board.

The AI-energy link is not a 2030 story. It is playing out right now, with direct implications for gas infrastructure, grid investment, and energy demand forecasts in every major market.

Disclamer- This content is for informational and educational purposes only and does not constitute investment, legal, or tax advice. Please consult qualified professionals before making any financial decisions. MintWit Financial Services LLP is an AMFI-registered Mutual Fund Distributor (ARN-283168); however, all investments are subject to market risks and returns are not assured.