The best time to plant a tree was 20 years ago.

The second best time is now.

The same logic, delightfully stubborn in its wisdom, applies to structuring your wealth. And once you’re navigating the rarified air of hundreds of millions (or even billions), the vehicle of choice becomes something far more exclusive, far more bespoke: a Family Office.

Let’s ground this in a scenario that’s becoming increasingly common in India’s entrepreneurial ecosystem.

Imagine this: You’ve just exited your company for $200 million. Champagne celebrations, congratulatory messages, and then… silence. You’re staring at a bank balance that could change the trajectory of generations.

The excitement is real. But so is the inevitable question:

What now? How do you preserve this capital, grow it, and ensure it benefits people you’ll never meet?

This is where a Family Office steps in.

At its simplest, a family office is a dedicated team of professionals on your payroll with one singular mission: protecting and compounding your family’s wealth across generations.

But its role is far more expansive than traditional investment advisory. This structure integrates investment management, tax strategy, estate planning, and legacy-building into one coordinated ecosystem.

It sets up trusts for tax-efficient transfers, designs philanthropic pathways that mirror your values, and builds succession frameworks that prevent the classic “third-generation wealth dilution.”

In short: it ensures your capital doesn’t just withstand market cycles or regulatory shiftS, it thrives, compounds, and creates a legacy that endures for decades, even centuries.

This month, we’re pulling back the curtain on Family Offices. We’ll explore:

1. From Rockefellers to Reliance: family offices evolve over centuries

2. The $100M Rule: when to launch a family office

3. Single, Multi, Virtual: choose your ideal family office model

4. The New Guard: first-gen entrepreneurs reshape wealth

5. Six trends defining India’s family office future

-

How Did These Offices Come Into Picture?

The concept of family offices emerged in 19th century Europe among aristocratic families who had accumulated substantial wealth over generations. However, it was in the United States where the modern family office truly took shape.

The Rockefeller family established Rockefeller Family & Associates in New York in 1882, creating what many consider the first modern family office. John D. Rockefeller, having amassed an extraordinary fortune from oil, recognized a fundamental truth: the skills required to create wealth differ entirely from those needed to preserve and grow it systematically. His family office became the template that subsequent wealthy families would study, adapt, and build upon.

J.P. Morgan & Co. further elevated the concept in the early 20th century. They expanded beyond basic wealth management to stabilize financial markets during economic crises, pioneer philanthropic frameworks that balanced social impact with family legacy, and establish governance structures for multigenerational wealth preservation. Their approach established principles that remain relevant today.

Now, let’s shift our lens to India, where the story unfolds quite differently.

While wealthy Indian families have always relied on trusted advisors, the family chartered accountant, the loyal lawyer, the investment-savvy relative, the formalized family office concept crystallized only after the 1991 economic liberalization. As India’s economy opened and industrialists and entrepreneurs began accumulating substantial wealth at unprecedented speed, informal advisory arrangements proved inadequate for the scale and complexity of modern wealth management.

Today’s Indian family offices have evolved from these informal networks into comprehensive wealth-management ecosystems built on three foundational pillars: preservation, growth, and legacy.

So, what exactly does a Family Office do today?

2. The $100 Million Question: When Does It Make Sense?

Let’s address this directly: Family offices aren’t for everyone. In fact, they’re suitable for only a small fraction of wealthy individuals.

Industry consensus, supported by economic analysis, suggests that $100 million in investable assets represents the minimum threshold for establishing a dedicated single family office. This figure isn’t arbitrary, it’s driven by the economics of scale required to justify the operational infrastructure.

According to the 2024 UBS Global Family Office Report, the average annual operating cost for a family office is approximately 0.4% of assets under management (AUM). For a family office managing $100 million, this translates to roughly $400,000 annually. This cost must be justified through superior investment returns, enhanced tax efficiency, comprehensive estate planning benefits, and the intangible value of coordinated wealth management.

The cost structure becomes more favorable as assets increase. While the average remains at 0.4% for AUM in the $100 million to $250 million range, it decreases to 0.35% for those managing over $1 billion. Fixed costs, personnel, technology, office infrastructure, get distributed across a larger asset base, improving overall efficiency.

The allocation of these costs reveals the operational anatomy: 57% goes to operational expenses including salaries for investment professionals, accountants, legal advisors, technology systems, and facilities. Another 24% covers asset management and advisory fees for specialized investment mandates. The remainder addresses compliance, specialized services, and technology platforms.

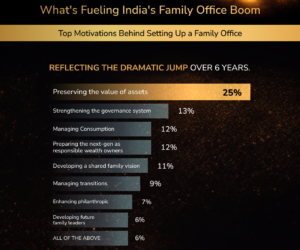

But here’s where numbers meet narrative. The decision to establish a family office isn’t purely financial. There are various reasons that can prompt families to set up a family office. In a recent Julius Baer-EY (JB-EY) study of more than 25 niche family offices in India, the leading reasons to emerge included the need for structured governance, centralized decision-making, and a more professional approach to managing growing financial complexity.

3. Single, Multi, or Virtual? Decoding the Different Models

Not all family offices operate identically. They exist on a spectrum from fully dedicated to efficiently shared. Understanding the three primary models is essential for making an informed choice.

Single Family Office (SFO): Full Control, High Cost

A Single Family Office is a dedicated entity built solely for one ultra-wealthy family. All professionals, investment managers, accountants, lawyers, estate planners, work exclusively for them. It offers maximum control, privacy, and fully customized wealth management.

However, it requires significant scale (typically $200M+), high fixed costs, and the commitment to run what is essentially a private wealth-management company.

Multi-Family Office (MFO): Shared Expertise, Lower Cost

An MFO serves multiple wealthy families under one institutional platform. By sharing infrastructure, technology, and talent, families access top-tier expertise at a fraction of SFO costs.

Ideal for families with ~$100M+, MFOs provide confidentiality, fiduciary oversight, and access to high-quality investment opportunities, though with slightly less customization than an SFO.

Virtual Family Office (VFO): Flexible, Outsourced Model

A VFO operates through a network of external specialists and digital tools instead of a full in-house team. It uses fractional CIOs, lawyers, advisors, and integrated technology to deliver coordinated wealth management with minimal fixed expenses.

Best for simpler structures or emerging wealth creators who want flexibility and efficiency without building a full office.

Setting up a family office starts with clarity on the family’s long-term vision and the level of control they want. Defining the purpose, whether wealth preservation, investments, philanthropy, or estate planning, shapes the office’s structure and services.

Clear roles, such as a Family Office Head and an Investment Committee, keep decisions coordinated and aligned with the family’s goals while technology and compliance systems support smooth day-to-day operations.

4. The New Guard: First-Generation Entrepreneurs Rewriting the Rules

And now, the plot thickens.

The family offices emerging across India today differ markedly from traditional models. Many are being established by first-generation entrepreneurs and investors, individuals who are younger, more comfortable with risk, digitally native, and possess deep expertise in emerging sectors that conventional wealth managers often struggle to understand.

These aren’t cautious inheritors of legacy wealth managing preservation. They’ve built fortunes through calculated risk-taking and data-driven decision-making, and they expect their family offices to operate with similar agility and innovation.

Today’s new-age UHNIs have outgrown traditional, standardised wealth approaches. They now expect solutions that are deeply personalised, innovative, and agile enough to adapt to fast-changing market dynamics.

The current assets under management (AUM) of India’s alternative investment industry, comprising Portfolio Management Services (PMS) and Alternative Investment Funds (AIFs), total approximately rupees 23.4 lakh crore as of September 2025. These assets are projected to exceed rupees 100 lakh crore by 2030, indicating robust growth in this sector driven by increasing investor interest and evolving regulatory frameworks. This projection highlights the rapid expansion and significant future potential of alternative investments in India.

Recent regulatory developments have accelerated this trend. SEBI has relaxed investment norms for Category II AIFs, the largest segment, allowing them to invest in listed debt securities with credit ratings of ‘A’ or below. This expands the investable universe substantially.

Budget 2025 provided additional impetus: sales of securities by AIFs will now be taxed as capital gains rather than business income. This change reduces compliance burden and improves after-tax returns for investors, a meaningful enhancement to the value proposition.

The appeal is grounded in performance data. SEBI reports and industry research indicate that boutique PMS and AIF managers focusing on emerging themes, micro-cap opportunities, digital inclusion, clean energy infrastructure, have demonstrated the ability to generate alpha that significantly outperforms broad market indices during sectoral growth phases.

Their competitive advantage lies in conducting differentiated research and taking concentrated positions that capitalize on market inefficiencies. These opportunities are often too small for large institutional funds but highly attractive for sophisticated family offices with patient capital.

The emerging investment philosophy among first-generation family offices is pragmatic: utilize mutual funds as the foundation for diversified, liquid exposure; deploy alternatives for alpha generation and thematic opportunities; reserve direct investments for sectors where family expertise provides genuine competitive advantage.

This represents wealth management reimagined for a new generation, sophisticated, nimble, and performance-focused.

5. The Road Ahead

Family offices have evolved beyond their original purpose of wealth management into institutions that bring structure, governance, and long-term thinking to how India’s ultra-wealthy approach capital, legacy, and societal responsibility.

They’re no longer simply about generating returns or minimizing taxes. They’re about creating integrated ecosystems that preserve wealth, facilitate smooth generational transitions, and generate lasting positive impact extending beyond the family itself.

The future appears promising as these institutions continue adapting, innovating, and leading in wealth stewardship. They’re establishing new standards for disciplined investment processes, rigorous governance frameworks, and holistic approaches that will shape family legacies for generations.

The ongoing challenge lies in capturing opportunities while maintaining unwavering commitment to core objectives: wealth preservation, sustainable growth, and legacy creation. A truly comprehensive approach encompassing strategy, technology, succession, governance, impact, and education will distinguish families whose wealth flourishes from those whose wealth diminishes over time.

After all, planting the tree is just the beginning. The real mastery lies in nurturing it through changing seasons, protecting it from threats, and ensuring it provides value for generations to come.

Disclaimer

This article is for informational purposes only. Data and insights are sourced from industry reports including UBS Global Family Office Report 2024, SEBI filings, and Julius Baer-EY research. While efforts have been made to ensure accuracy, readers should conduct their own research and consult qualified professionals before making financial decisions. References to entities and investment vehicles are illustrative and not endorsements.