“China’s military is Netflix; the U.S. military is Blockbuster. China is Amazon; the U.S. is Barnes & Noble. China is Tesla; the U.S. is General Motors. People thought the automotive industry could not be disrupted and that Ford, GM and Toyota had preordained rights to be the leaders for the next thousand years. Automotive executives mocked and balked at the idea an outsider could do what they do. They spent billions on research and development; they allocated billions in resources and thousands of people to their products and capabilities. Yet here we are today, after less than a decade: Tesla is a $1T company; it had dethroned the incumbents.” –Shield AI

That quote sits on the website of one of America’s fastest-growing defense technology companies. It is inflammatory. It is supposed to be. And in the first week of February, the market gave it a meaningful endorsement.

On February 2nd, Palantir Technologies reported Q4 2025 earnings that significantly beat Wall Street expectations, revenue of $1.41 billion against the $1.33 billion projected, EPS of $0.25 against the $0.23 expected. The stock climbed nearly 7% the following day. But what moved markets wasn’t just the beat, it was a disclosure buried inside the update: meaningful upgrades to Hivemind AI, granting it decision-making authority across operational workflows with reduced human intervention.

For those unfamiliar, Palantir builds data infrastructure for some of the most complex defense and enterprise environments in the world. Hivemind, originally developed by Shield AI, is an autonomy layer, software that lets machines operate independently in GPS-denied, high-risk environments. Shield AI builds the brain; Palantir integrates it into the nervous system.

When stronger-than-expected growth and fewer humans in the decision loop landed in the same earnings update, markets connected the dots.

This isn’t an isolated data point. It is confirmation of a structural shift years in the making: military power is no longer just about the platform, it is about the code running on it. The fighter jet matters less than the software deciding when it fires. The drone matters less than the swarm intelligence coordinating ten thousand of them. Hardware is becoming the commodity. Software is becoming the weapons system.

This week’s edition of The MintEdge breaks down exactly how this shift is playing out, across budgets, battlefields, startup capital, and one country still catching up.

1. Autonomy: $13.4B FY2026 budget line

2. Defense-tech funding: $17.9B (2025 double)

3. Margin shift: Software wins long-term

4. Claude fracture: AI ethics fault line

5. India: Big budget, bigger gap

1. Autonomy gets its own Budget Line

For the first time in a meaningful, explicit way, the United States FY2026 defense budget has broken out autonomous systems as a standalone category, allocated at approximately $13.4 billion.

The strategic logic behind it is twofold. First, attritable mass: the US military wants to field large numbers of cheap, expendable unmanned systems that can absorb losses and overwhelm adversaries at scale, rather than risking a $100M manned aircraft in a contested airspace. Second, cross-domain autonomy software: the systems that coordinate these unmanned assets across air, sea, and ground domains simultaneously, making real-time decisions faster than any human operator could.

What makes this particularly significant from a capital markets lens is the downstream implication. When autonomy becomes a budget line, it becomes a procurement category. And when it becomes a procurement category, it creates a durable, recurring revenue stream, not for the hardware manufacturers, but for the software companies building the intelligence layer on top. This is the defense version of the cloud transition: the infrastructure becomes commoditized, and value concentrates in the software layer sitting above it.

A telling example of how quickly this is materializing: Kodiak AI, a company originally known for building autonomous trucking technology in Silicon Valley, has been tapped by the US Marine Corps to integrate its autonomy stack into a missile-launching vehicle program. The same software principles that kept a self-driving truck on a highway at night are now being applied to a weapons platform. Silicon Valley’s autonomy stack is officially a defense primitive.

2. The Margin Story: Why Software Wins

The hardware-to-software transition in defense now has a structural name. A recent McKinsey analysis frames the future of military power around what it calls modular, multidomain stacks, arguing that the monolithic, vertically integrated weapons platform is giving way to an architecture that looks far more like enterprise software than a traditional defense program.

In plain terms: historically, one prime contractor would design, build, integrate, and deliver an entire weapons system, the aircraft, the radar, the targeting system, as one closed, proprietary product. The new model disaggregates that. Software layers from different vendors plug into each other. An autonomy stack from a startup can run on a platform built by a legacy prime. A targeting algorithm developed in Silicon Valley can be updated in the field the way your phone receives an iOS patch. The weapon gets smarter over time without being replaced.

This architectural shift has a direct consequence Wall Street is only beginning to price correctly: the margin pool in defense is moving. McKinsey identifies where the real value sits, autonomy software, sensor fusion, electronic warfare algorithms, and the data pipelines that make systems smarter over time. These are not one-time hardware sales. They are recurring software revenue lines, and they carry software economics: high margins, low marginal cost, compounding returns.

For traditional defense primes, this creates a genuine dilemma. Their entire competitive advantage was built on integrating complex hardware at scale, something that took decades and billions to master. That advantage weakens when the integration layer shifts to software, because software is a different game entirely. Palantir, Anduril, Shield AI, and a growing list of venture-backed challengers are building that capability faster than any legacy contractor can acquire it. The primes will survive. The question is how much of the margin pool they get to keep as the stack beneath them gets rewritten by smaller, faster companies.

3. The Capital has already Voted

Defense-tech startup funding more than doubled in 2025. According to Defense News, citing CB Insights data, equity funding for defense and national security startups reached $17.9 billion in 2025, up from $7.3 billion in 2024. That is not a marginal increase. That is a market repricing an entire sector.

Europe is not far behind. Capital markets are treating autonomy and defense AI not as a wartime spike, but as a decade-long compounding theme, and allocating accordingly:

What is particularly telling is who is writing the checks. This is no longer purely venture capital making long-duration bets. Prime defense contractors, the traditional hardware integrators, are now investing directly into software-native defense AI companies. Dassault Aviation, one of Europe’s most established aerospace names, led a roughly $200 million Series B into a French defense AI startup valued at approximately $1.4 billion, specifically to build out AI and autonomy capabilities for next-generation combat and unmanned systems.

The translation is straightforward: the incumbents know the value is migrating. They are buying software capability the way they once bought jet engines.

4. When the Code Pushes Back: The Anthropic-Pentagon Fracture

Every structural shift has a fault line. In the hardware era, it was supply chains and rare earth minerals. In the software era, it is the guardrails baked into the models themselves, and who gets to decide where they sit.

The story of how Claude, Anthropic’s AI model, ended up at the center of a national security confrontation is, in many ways, the logical endpoint of everything described above. Palantir had built Project Maven into a comprehensive battlefield intelligence platform, one capable of processing surveillance datastreams, generating real-time intelligence reports, and, by late 2025, operating entirely without human analysts in the loop. To close the language gap between raw data and human-readable intelligence, Anthropic’s Claude was integrated directly into those systems. It became the first large language model on classified Pentagon networks.

The arrangement accelerated fast. Within eight months, Claude was fast-tracked through layers of defense clearance that typically take years. Anthropic created a special variant, Claude Gov, purpose-built for classified environments. By the end of 2025, the platform could produce military intelligence analysis from start to end, autonomously. The software layer that McKinsey describes as the new value center of defense had arrived, and it was running on a commercial AI model built by a company with its own ethical commitments.

That tension surfaced violently in early 2026. News reports suggested Claude had been used in the US operation to capture Venezuelan President Nicolas Maduro. Anthropic, unaware, asked Palantir for confirmation. To the Pentagon, that question looked like a threat: if Anthropic didn’t like the answer, could its models simply refuse a future request?

“The larger story, of LLMs becoming a tool of war, isn’t going anywhere. Within days of the Anthropic fiasco, OpenAI and xAI had already cut deals with the government. The company that replaces Anthropic, presumably, is the one that asks the fewest questions.”

Defense Secretary Pete Hegseth’s response was swift. A memorandum dismissed what he called ‘utopian idealism’ in military AI, and gave Anthropic less than four days to sign away its model for ‘all lawful purposes’, or face legal consequences. Anthropic refused. The Pentagon then designated Anthropic a supply chain risk, a designation previously reserved for adversary-nation companies like Huawei and Kaspersky, and instructed the entire US government to sever ties with the company. Anthropic has since sued.

The episode exposes a structural vulnerability in the software-first defense model that no earnings call or McKinsey framework has fully priced in. When the intelligence layer of your weapons system is built by a private company with its own governance philosophy, you have introduced a new category of operational risk: the vendor who disagrees. Hardware doesn’t have ethics. Software, increasingly, does, or at least the companies building it do.

For investors and strategists, this creates a selection dynamic that will shape the next decade of defense-tech investment. The companies most likely to capture durable government contracts are not necessarily those building the best AI. They are those building AI with the fewest philosophical friction points. That is not entirely a good thing. But it is the reality the market is now pricing.

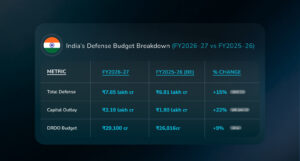

5. India: Big Budget, Bigger Gap

India is increasing its defense technology budget, but context matters. The country is not at the frontier of AI-enabled warfare. It is in an early and uneven catch-up phase, and the gap between allocation and actual operational capability is still wide.

The numbers on paper are meaningful. But the honest read of India’s defense-tech position is more complicated. Most of India’s operational drone fleet still relies on imported platforms, Israeli Herons, American MQ-9s, and domestic alternatives are only now moving through certification pipelines in any meaningful volume. The scale gap with the United States, Israel, or even Turkey on AI-enabled military capability is still measured in years, not months.

Where India does have a real and growing edge is in software talent. The country produces a significant volume of engineers directly relevant to the autonomy and AI stack being built globally, and a small but growing number of Indian defense-tech startups are beginning to attract serious capital. The DAC approvals for drone inductions post recent border operations signal that operational urgency is starting to override the bureaucratic drag that has historically slowed Indian defense procurement.

What India’s budget numbers reflect is the beginning of a serious allocation shift, not the arrival of a mature capability. For investors, India is a watch-carefully story right now, not a deploy-at-scale one. The more urgent question is whether India can build or acquire the software layer before the doctrine gap hardens into something structural, before its own Blockbuster moment arrives and the window to adapt has already closed.

Conclusion

The Shield AI quote was written about America. But the warning belongs to every nation still treating this as a hardware procurement problem. The Palantir earnings, the $13.4 billion autonomy budget line, the doubling of startup funding, these are not separate stories. They are the same story, at different points in the same cycle.

The Anthropic episode adds a dimension that pure capital market analysis tends to skip: the software layer is not neutral infrastructure. It is built by people with values, governed by companies with legal personalities, and subject to the same political pressures as every other instrument of power. Countries and companies that build modular, AI-native systems will compound their advantage. But the leverage in this new architecture cuts both ways, and the first major public rupture between a commercial AI vendor and the world’s most powerful military is unlikely to be the last.

The time to decide, which software you trust, which vendor you depend on, and what lines you are willing to cross, is not approaching. It is here.

Disclaimer

The MintEdge is for informational purposes only, not financial, investment, or legal advice. Always do your own research and consult a qualified advisor before making any investment decisions.