The world’s waste trade is collapsing on paper. In reality, it’s just been reborn, as a geopolitical contest over who gets to keep the good stuff.

Every city in the world produces waste. Mountains of it, plastic bottles, old electronics, corrugated cardboard, scrap metal, food packaging. Most of it ends up in one of three places: a landfill, an incinerator, or a recycling facility. But for decades, there was a fourth option that most people never thought about, and it quietly became a multi-billion dollar global industry. Countries simply shipped their trash to other countries.

This wasn’t dumping in the criminal sense, at least not always. It was trade, governed by contracts, shipping manifests, and customs codes. The logic was straightforward: rich countries produced more waste than they could cheaply process, and poorer manufacturing nations had the cheap labour and industrial appetite to sort, clean, and convert that waste into usable raw material. One man’s trash, as the saying goes, is another man’s treasure. For a long time, that wasn’t just a saying. It was an entire industry’s business model.

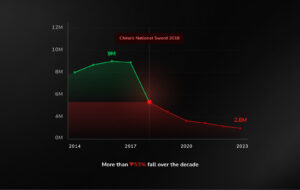

Then, early this decade, something broke. Global plastic waste trade fell sharply, from about 12.4 million tonnes in 2014 to 5.8 million tonnes in 2023, nearly halved. Regulators are cheering. Environmentalists are cautiously optimistic. But look closer, and this story is far messier, far more interesting, and far more consequential than a falling chart suggests.

In this week’s edition of The Mint Edge we cover-

1. The world’s dirty outsourcing machine

2. The recycling lie

3. Why scrap suddenly became strategic

4. The critical minerals race happening above ground

5. India’s hidden industrial asset

6. Why waste is the new climate infrastructure

1. The world’s dirty outsourcing machine

For most of the 1990s and 2000s, the waste trade solved a real problem on both sides.

Rich countries generated huge volumes of mixed waste. Processing it at home was expensive: labour costs, environmental rules, political resistance to landfills and incinerators. Sending it abroad was simply cheaper.

Manufacturing hubs across Asia had cheap labour, rising industrial demand, and the ability to extract usable materials from discarded plastics, metals, and paper. What looked like garbage in one country was low-cost feedstock in another.

China sat at the centre of this system. By 2016, it was absorbing roughly 56% of the world’s traded plastic waste. For Western economies, exporting waste made recycling targets look great on paper. For China, “foreign garbage” fuelled its manufacturing engine.

The economics worked partly because nobody wanted to look too closely. A large share of what was labelled “recyclable” was contaminated: food-soiled packaging, multilayer plastics, mixed materials, low-value residue that could not realistically be recycled. Much of the world’s “recycling” was outsourced waste disposal dressed up in green language.

The environmental cost just landed somewhere else.

2. The recycling lie

By 2018, China had had enough.

Its National Sword policy banned 24 categories of solid waste imports and dropped contamination thresholds from 5–10% down to 0.5%. Effectively another ban. The economics of the global waste trade broke overnight.

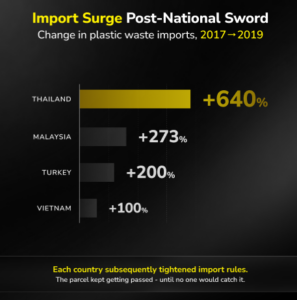

The flow rerouted into Southeast Asia. Malaysia’s imports surged. Thailand exploded. Indonesia and Vietnam became new hubs. Within two or three years, they too were shutting their doors.

Then came Basel. The Basel Convention’s plastic waste amendments, agreed in 2019 and in force from January 2021, brought most plastic waste under prior informed consent. Contaminated mixed plastic could no longer move internationally without explicit government approval on both ends of the journey.

On paper, this looked like progress. Global plastic waste trade fell from around 12.4 million tonnes in 2014 to about 5.8 million tonnes in 2023.

The reality is messier.

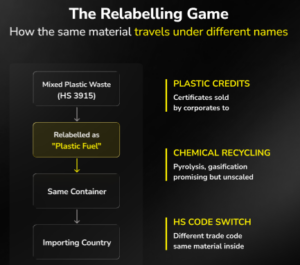

A lot of the same material started moving under different labels: “fuel,” “used goods,” “plastic pellets,” or completely different customs classifications. The trash didn’t disappear. It just changed names.

A more sophisticated layer has now emerged: the financialisation of recycling itself. Plastic credits and carbon-linked recycling markets are becoming a serious ESG asset class. Companies buy certificates claiming equivalent amounts of plastic have been recovered somewhere else, often in countries that have no formal waste infrastructure to speak of.

Defenders argue these mechanisms fund collection where governments have failed. Critics argue it is the old outsourcing logic in a sustainability costume, monetised through climate accounting. Honestly, both are right.

3. Why scrap suddenly became strategic

Plastic is being squeezed out of global trade. Scrap metal is moving the other way. The reason is climate.

Traditional blast furnaces burn coking coal and emit roughly 2 tonnes of CO₂ per tonne of steel. Electric Arc Furnaces (EAFs) run on scrap and emit a fraction of that. As steel buyers, particularly in Europe, start demanding lower-carbon supply, the value of discarded steel changes completely. It is no longer waste. It is feedstock for green industry.

Turkey, the world’s largest scrap importer, brought in close to 19 million tonnes of ferrous scrap in 2023, and 20.09 million tonnes in 2024. India, the second-largest, brought in roughly 11 million tonnes in calendar year 2023, up 40% year-on-year. MRAI estimates India’s total scrap demand could touch 65 million tonnes annually by 2030.

Developed economies are turning protectionist. In October 2025, the US Aluminum Association released a white paper calling for an immediate ban on Used Beverage Container (UBC) exports outside North America. UBCs are the highest-grade aluminium scrap. A can recycled into a new can takes about 60 days and roughly 5% of the energy of primary production. The association also pointed out that China, India, Russia, and Saudi Arabia already restrict UBC exports. The US, it argued, was being naive.

Europe is moving the same way. From 21 November 2026, the EU will ban plastic waste exports to non-OECD countries outright, for at least two and a half years. Industrial lobbies inside the bloc are now pushing for similar restrictions on scrap metal, especially with the Carbon Border Adjustment Mechanism (CBAM) entering full enforcement in 2026. The logic is straightforward: if EU producers will pay a carbon penalty on imported steel, they would much rather keep cheap, low-carbon scrap inside the bloc than ship it to Turkey or India to make competing rebar.

The pattern is clear. For decades, waste was exported because it was dirty and low-value. Decarbonisation flipped that. The same scrap once shipped out cheaply is now essential for green steel, low-carbon manufacturing, and energy-efficient production.

The world is quietly entering an era of resource nationalism. Except this time it is for the stuff coming out of bins, not mines.

4. The critical minerals race happening above ground

The geopolitics gets sharper when you move from steel to batteries.

A modern lithium-ion battery contains lithium, cobalt, nickel, manganese, copper, and trace rare earths. India imports nearly all of these. China controls between 60% and 90% of the world’s processing capacity across these minerals depending on which one you pick. The “China risk” in EV supply chains is not really about mining. It is about refining.

Which means the next mining boom is happening above ground. In discarded laptops. Old scooter batteries. Server racks. End-of-life EVs.

A few numbers explain why this matters for India. MRAI estimates the country will need 65 million tonnes of scrap a year by 2030 and domestic generation may cover only half. The rest has to come from imports, if other countries don’t shut the tap first.

So we are looking at a strange new race. Countries that don’t have lithium mines or nickel deposits are now building national stockpiles by mining their own e-waste. Urban mining is no longer a futuristic phrase. Japan officially calls its e-waste reserves “urban mines” in policy documents. China has been building integrated lithium-battery recycling capacity at scale since 2018. India is, frankly, behind.

This is where the investment opportunity quietly hides. Critical-mineral recycling is moving from a sustainability-themed bet into a strategic supply-chain bet. That is a very different multiple to pay.

5. India’s hidden industrial asset

India sits at a strange and potentially powerful crossroads.

It banned plastic waste imports in August 2019, then partially walked it back through SEZ exemptions and later policy tweaks. It is one of the world’s largest importers of ferrous scrap. And it already has something most developed economies don’t: a deeply embedded informal recycling network.

The kabadiwala economy, itinerant collectors, neighbourhood aggregators, sorters, dismantlers, small processors, recovers materials at a scale and granularity most formal Western systems can’t match. Industry estimates put the informal layer at 95–99% of India’s actual recycling activity. Almost none of it shows up in formal climate accounting or industrial statistics.

A new generation of Indian companies is now trying to industrialise the sector around that base.

Attero, founded in 2008 in Dehradun, is one of the largest electronic-asset and lithium-ion battery recyclers in the country. It recovers over 98% of metals like lithium, cobalt, and nickel, holds 46+ global patents, and now exports its technology to Europe, the Middle East, and Africa.

Recyclekaro runs one of India’s largest Li-ion battery recycling facilities near Mumbai. 17 acres in Palghar. Plans to scale processing capacity to roughly 50,000 tonnes. Recently licensed extraction technology from IIT Bombay.

PolyCycl is working on chemical recycling for plastics that mechanical recycling cannot economically handle. Recove is focused on formalising circular manufacturing ecosystems and Extended Producer Responsibility (EPR) traceability.

The opportunity here is bigger than waste management.

India already has labour, waste volume, collection density, manufacturing ambition, and possibly the world’s largest decentralised recovery system already operating quietly in every Indian city. The honest question is whether it formalises this advantage before the rest of the world locks down its own recyclables. Because that window is not staying open forever. The EU’s November 2026 plastic export ban is one signal. Scrap restrictions across developed markets are another. Secondary raw materials are being treated as strategic inputs now, not disposable excess.

Could India become to recycled materials what China became to manufacturing?

The answer may shape an entire industrial sector over the next two decades. My honest take: yes, it is genuinely possible, but only if India formalises the kabadiwala economy rather than trying to replace it with imported Western models. The base layer is already world-class. What’s missing is the tech, capital, and traceability stack on top.

Pull all of this together and the waste trade stops being a sustainability story. It becomes something much bigger.

It is now simultaneously:

– climate policy, because recycled materials cut emissions

– industrial strategy, because secondary raw materials feed green manufacturing

– carbon accounting, because credits are being built around them

– supply-chain security, because they reduce import dependence

– resource geopolitics, because countries that hoard them gain leverage

For thirty years, globalisation moved waste outward. The next thirty may move recyclable resources inward.

In a decarbonising world, recycled steel cuts emissions, recycled aluminium saves enormous amounts of energy, battery recycling improves mineral security, and circular manufacturing reduces dependence on volatile commodity imports.

Waste is no longer something societies throw away. It is industrial inventory.

The countries that build serious recycling ecosystems today will probably control cheaper, greener material supply chains tomorrow. The ones that fail may find themselves importing back the very materials they once discarded, at premium prices, from competitors.

Disclaimer

This content is for informational and educational purposes only and does not constitute investment, legal, or tax advice. Please consult qualified professionals before making any financial decisions. MintWit Financial Services LLP is an AMFI-registered Mutual Fund Distributor (ARN-283168); however, all investments are subject to market risks and returns are not assured.