A Berkshire Hathaway vice-chairman flew from the United States to Delhi to personally close a real estate deal. For those who understand how investment-disciplined the people around Warren Buffett are, that detail alone tells the story. The address was Gurugram. The amount was rupees 85 crore. The signal was not about one apartment, it was about the decade of price discovery ahead.

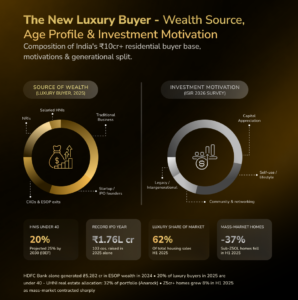

India’s ultra-rich population is growing rapidly and reshaping the country’s premium markets. The Hurun Global Rich List 2026 reports 308 Indian billionaires, 24 more than last year, making India the third-largest billionaire hub after the US and China. Meanwhile, Capgemini’s World Wealth Report 2025 estimates that Indian HNWI wealth has reached about $1.5 trillion, with the country seeing some of the fastest growth in millionaires globally. Twenty percent of this wealth class is now under forty, first-generation founders, ESOP millionaires, and IPO beneficiaries who have compressed a generation of wealth-building into a single decade of India’s digital economy.

The real estate sector absorbs the largest single share of this capital, 32% of UHNI portfolios by allocation, according to Anarock. And within real estate, the gravitational centre has quietly, decisively shifted. For the first time in the history of modern Indian premium property, a city outside Mumbai leads total luxury home sales. Gurugram recorded rupees 24,120 crore in transactions for homes priced above rupees 10 crore in 2025, against Mumbai’s rupees 21,902 crore in the same segment. The margin is not close. The speed at which it opened is almost without precedent.

This edition of The Mint Edge maps the structural forces driving that shift: the new wealth class that is writing the demand, the economics of global price convergence, the infrastructure compounding that makes Gurugram’s trajectory durable, and what the data says about where the next price cycle is likely to go.

1. The Scoreboard- How the numbers moved and what the velocity tells

2. The Address as Social Capital- the real ROI of India’s billionaire

3. The NRI Repatriation Trade, $135 billion in remittances and the currency logic

4. The Price Discovery Gap, why Indian luxury is still structurally cheap vs global peers

5. The New Wealth Behind the Wave- who is actually buying and what drives them

1. The Scoreboard: How the Numbers Moved, and What the Velocity Tells Us

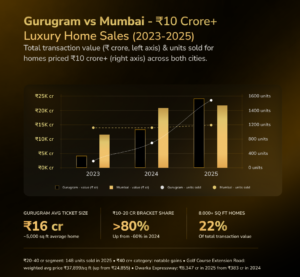

The India Sotheby’s International Realty and CRE Matrix joint report, published in February 2026, is the most consequential piece of real estate data to emerge from India in years. Not because the absolute numbers are the largest ever, though they are, but because of the rate at which Gurugram’s luxury market has compounded. In 2023, the city sold 155 homes priced above rupees 10 crore, totalling rupees 4,004 crore. In 2025, it sold 1,494 homes totalling rupees 24,120 crore. That is a near-tenfold rise in volume and a six-fold rise in value, achieved in 24 months, in a segment that globally is defined by its resistance to rapid change.

For context: Mumbai sold 924 ultra-luxury units in 2024, reaching rupees 20,415 crore. In 2025, it sold 967 units at rupees 21,902 crore, a 4.7% rise in unit volume and a 7.3% rise in value. That is a healthy, stable premium market performing broadly in line with expectations. Gurugram’s 188% rise in units and 80% rise in value against those same benchmarks is not a cyclical move. It is a structural re-rating.

The tier breakdown within Gurugram’s luxury segment is also instructive. The rupees 10–20 crore bracket now accounts for over 80% of units, up from 60% in 2024. This is not a market driven purely by outlier trophy transactions. It is a broad-based demand shift across an entire price tier, which historically signals that a market is entering a phase of sustained appreciation rather than speculative spike. The 148 units transacted in the rupees 20-40 crore bracket, and meaningful activity above rupees 40 crore, confirm that the top end of the pyramid is thickening simultaneously.

What makes Gurugram’s 2025 performance even more striking is that it occurred against a backdrop of significant headwinds in the broader listed real estate sector. The Nifty Realty Index fell 14–20% over the same period as regulatory pressures and liquidity concerns weighed on listed developers. The divergence between Gurugram’s ultra-luxury market and the broader sector is one of the sharpest signals in recent Indian real estate history, it suggests the demand is coming from a buyer cohort that is entirely decoupled from the broader housing market and its cyclical pressures.

2. The Address as Social Capital

The Berkshire executive who flew to Delhi to close the Camellias deal was not making a lifestyle decision. He was making an allocation, and the most valuable asset in that allocation was not the 7,400 square feet of floor space. It was the address itself, and what that address grants access to. DLF Camellias on Golf Course Road has quietly become the most concentrated gathering of India’s entrepreneurial wealth under a single residential roof. The building is less a luxury apartment complex and more a physical manifestation of the networks that now govern capital flows in Indian business.

India Sotheby’s survey data supports this directly: 44% of HNIs cite community and networking as a primary driver of ultra-luxury residential purchase, the second-highest motivation after capital appreciation. For UHNIs specifically, this figure is likely higher, because the returns from serendipitous proximity are non-linear. The kind of deal flow, co-investment opportunities, and relationship capital that a founder acquires by sharing a building with India’s top DTC entrepreneurs, fintech operators, and institutional investors cannot be replicated by any club membership or conference circuit. The address is doing work that cannot be purchased any other way.

There is a documented global parallel for what is happening here. Manhattan’s 220 Central Park South and London’s One Hyde Park do not command their premiums purely because of the views or the concierge service. They command them because the buyer cohort itself becomes the asset. The term of art in global wealth circles is “co-location premium”, the measurable uplift in deal velocity, information access, and network density that accrues to residents of buildings where capital density exceeds a certain threshold. India now has its equivalent. The Camellias resident list is a more concentrated gathering of Indian tech and consumer internet wealth than most industry conferences.

This dynamic also creates a self-reinforcing cycle that is structurally different from conventional real estate appreciation. As each high-profile buyer joins, the address becomes more valuable to the next buyer, not because the building has changed, but because the network it provides access to has deepened. The building was nearly sold out before secondary market interest fully priced in this network effect. For the cohort that bought early, the capital appreciation has been both financial and social.

3. The NRI Repatriation Trade: $135 Billion Looking for a Home

India received $135.46 billion in inward remittances in FY25, a 14% jump year-on-year and a new record, confirmed by the Reserve Bank of India. To contextualise the scale: India now receives more in annual remittances than the GDP of Morocco. This figure has more than doubled from $61 billion eight years ago, and every structural indicator suggests it has not peaked. The number of Indians holding senior positions in global corporations, building businesses abroad, and reaching ESOP liquidity events in foreign currency is growing faster than at any prior point in history.

A growing, trackable share of this capital is returning to Indian real estate, and it is arriving disproportionately in the ultra-luxury segment. NRIs contributed an estimated 20% of India’s total real estate investment in 2025, up from 7–10% in 2015–18. At DLF specifically, NRI sales went from 5% of total sales in FY22 to 14% in FY23 to 23% in FY24. The trajectory at Camellias, which already counts a Singapore tycoon, a British businessman, and the Berkshire executive among its recent buyers, is steeper still.

The economics driving this repatriation are structural rather than sentimental, though sentiment plays a role too. Consider the core arbitrage: an rupees 85 crore apartment on Golf Course Road is approximately $10 million at current exchange rates. The rupee has depreciated 15–20% against major currencies since 2020, meaning the effective cost in foreign currency terms has fallen even as the rupee price has appreciated. A comparable gated luxury address in Singapore or London runs $20-30 million for equivalent square footage. The NRI buyer is not returning home out of nostalgia. They are executing a sophisticated global asset allocation trade in which Indian ultra-luxury real estate offers London-quality product at a structural discount that has several more years of convergence ahead of it.

There is also a consolidation dynamic at play. NRI portfolios built over the 1990s and 2000s tend to be fragmented, a 2BHK in Andheri, an older flat in their hometown, a commercial space somewhere in between. The new ultra-luxury addresses offer an exit from that fragmentation. Sell the portfolio, centralise the capital, and buy a single professionally managed, globally benchmarked address in the building where the next ten years of Indian deal flow will be happening. The appeal is not hard to understand.

4. The Price Discovery Gap: Why Indian Luxury Is Still Structurally Cheap

The most important macro insight in India’s luxury real estate story is not what has already happened, it is the gap between where prices are and where they should converge to, given the UHNI density and economic weight India is accumulating. Gurugram’s best addresses now trade at approximately rupees 1–1.1 lakh per square foot, or roughly $1,200–$1,300. By any global comparison with cities of comparable corporate density and wealth concentration, that number is strikingly low. Dubai’s prime residential corridors trade at $3,500–5,000 per square foot. Singapore’s Orchard and Marina Bay addresses are at $4,500–6,000. London’s prime central market sits at $7,000–10,000. Monaco is in a different atmosphere entirely.

The implication is not that Gurugram should reach Monaco. It is that even a partial convergence to the level of, say, Dubai or Singapore, cities with a fraction of India’s UHNI base, implies a 2.5x to 4x move in per-square-foot pricing from current levels. The structural case for Indian luxury real estate over the next decade is not built on sentiment or momentum. It is built on the mathematics of wealth density versus price per square foot, and the gap between those two numbers is larger in India than in almost any other major economy.

Mumbai’s per-square-foot story is nuanced differently. The city already trades at London adjacency in its best micro-markets, Malabar Hill, Worli, Altamount Road, which is partly why its growth has plateaued at the top. Gurugram, by contrast, is still in the earlier phase of its price discovery. The infrastructure build-out compounding beneath the market makes the case even stronger. The Delhi–Mumbai Expressway, India’s longest, now operational, terminates effectively at Gurugram’s doorstep. The Jewar International Airport, projected to become one of Asia’s largest, is under construction 40 kilometres from Golf Course Road and will reshape the region’s connectivity in ways that are not yet priced into current valuations. The NH-48 expansion, the Dwarka Expressway metro extension, and the proposed Regional Rapid Transit System together form an infrastructure stack that most global cities would consider remarkable.

For investors, the asymmetry in the Gurugram trade is straightforward. You are buying into a market that is simultaneously: underpriced relative to global UHNI density, experiencing demand acceleration across multiple buyer cohorts, and about to receive infrastructure upgrades that typically trigger 20–40% valuation re-ratings in comparable global markets. The window where all three of these conditions are simultaneously true is not indefinite.

5. Young, Tech-Rich, Globally Wired: The New Wealth Behind the Wave

India’s luxury buyer profile has changed more in the last five years than in the preceding two decades. Traditional business families and industrial scions remain part of the mix, but they are no longer the defining cohort. The decisive shift is the arrival, at scale, of a new class of wealth: startup founders whose companies have gone public, senior professionals sitting on crores of vested equity, and a generation of young entrepreneurs who built companies during India’s digital decade and have emerged with the kind of capital that previously took an entire lifetime to accumulate.

In 2025, 103 Indian companies raised rupees 1.76 lakh crore through IPOs, a single-year record. That capital did not sit idle. Wealth managers who serve this cohort report a consistent pattern: within twelve to eighteen months of a major liquidity event, a meaningful portion moves into luxury real estate. The reasoning is intuitive and also culturally deep. For a founder who has spent years watching equity valuations on a spreadsheet, a physical asset with a prestigious address represents permanence, an anchor in the material world that volatile financial assets cannot provide. India Sotheby’s 2026 Outlook Survey captures this precisely: 47% of luxury buyers in 2025 cited self-use and lifestyle as primary motivations, up significantly from prior years. The new buyer is not purely an investor. They are also a resident.

What distinguishes this generation from prior luxury buyer cohorts is their reference frame. They did not grow up aspiring to a Lutyens bungalow or a sea-facing flat in South Mumbai. They built their companies in Gurugram, raised capital in Gurugram, recruited their teams in Gurugram, and watched their networks consolidate in Gurugram. Their standard of comparison for a home is not the Indian market of a generation ago, it is the Marina Bay Sands penthouse, the Belgravia townhouse, the Downtown Dubai high-rise. When Indian product achieves that standard at a fraction of the global price, the purchasing decision is not emotional. It is rational.

There is also a wealth preservation logic at work that is specific to this cohort. A founder who holds significant equity in a single company, however successful, is exposed to concentration risk that is uncomfortable by any portfolio management standard. Real estate, specifically ultra-luxury real estate in a market experiencing structural re-rating, provides both diversification and the kind of tangible, generational permanence that a stock certificate cannot. The 32% real estate allocation in UHNI portfolios is not accidental. It reflects a considered view that physical assets in appreciating micro-markets are among the most reliable stores of wealth available in the Indian context.

What This Means for You

Wealth does not travel far from where it is made. It consolidates, compounds, and eventually crystallises in the places where the people who created it choose to live. Gurugram’s rise to India’s premier luxury address is not a coincidence of geography, it is the logical endpoint of a decade in which India’s most consequential companies, capital markets, and career trajectories all ran through the same postal codes. The city became the engine. The real estate followed the engine.

That principle, where wealth is created, it is eventually reflected, is the most useful lens for understanding what comes next. Because Gurugram is no longer an emerging story. It is a discovered one. The buyers who moved earliest are sitting on positions that a 2022 market participant would have called aggressive. They were not aggressive. They were early.

Which raises the only question that matters now: where is the next Gurugram?

The answer is not a single city. It is a pattern. And that pattern is already visible in places that are building their own versions of the same story, new corporate clusters, compressing infrastructure, first-generation wealth with no inherited preference for the old addresses. We explored this shift in an earlier edition: the quiet but unmistakable rise of India’s tier 2 cities as genuine wealth destinations, not feeder markets. That story is worth revisiting.

For anyone thinking seriously about where capital should be positioned in Indian real estate over the next cycle, the variables to watch remain the same: infrastructure triggers not yet priced in, IPO-driven liquidity looking for a physical anchor, and the secondary market premiums that signal where the next re-rating begins. The window in any market where all three align is narrow. In Gurugram, that window is closing. Somewhere else, it is just opening.

The question is not whether you believe in India’s wealth story. That debate is settled. The question is whether you are positioned in the right address for the next chapter of it.

Disclaimer

The MintEdge is for informational purposes only, not financial, investment, or legal advice. Always do your own research and consult a qualified advisor before making any investment decisions.