Twenty years of negotiations. Eighteen rounds of talks. One week after America slapped 50% tariffs on Indian exports.

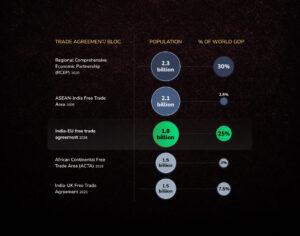

On January 27, 2026, India and the European Union announced the conclusion of what both sides are calling “the mother of all deals”: a free trade agreement that creates a market of 2 billion people, covers 25% of global GDP, and fundamentally reshapes how the world’s largest democracy and its biggest democratic bloc do business.

The timing? Deliberate. The stakes? Existential.

With the US imposing crippling 50% tariffs on Indian textiles, gems, jewellery, and leather goods, India’s $86.5 billion annual exports to America faced near-total collapse. The textile sector alone braced for a 70% export drop. Meanwhile, the EU watched Trump threaten geopolitical instability across the Atlantic.

Neither side was negotiating from weakness. They were negotiating from necessity.

This month, we dissect the India-EU FTA. We cover:

1. The 18-year journey from ambition to agreement

2. What each side appears to have won based on announcements

3. The sectors poised for explosive growth

4. How this reshapes India’s tariff crisis with America

5. The execution challenge: turning promises into prosperity

1. From 2007 to 2026: The Deal That Refused to Die

The story begins in 2007, when India and the EU launched FTA negotiations during a different era of globalization. The world was optimistic about free trade. China was joining WTO. Supply chains seemed permanent.

Then reality intervened. Talks stalled in 2013 over irreconcilable differences: the EU demanded dairy market access and lower auto tariffs; India wanted easier visa rules for IT professionals and protection for its farmers. For nine years, the negotiations went dormant. Not dead, dormant.

What changed in 2022? Everything.

Russia’s invasion of Ukraine shattered Europe’s energy security assumptions. The EU, suddenly desperate to diversify supply chains away from China and secure reliable partners, looked east. India, navigating a complex geopolitical landscape while maintaining strategic autonomy, saw an opportunity to deepen economic ties without compromising sovereignty.

Prime Minister Modi and European Commission President Ursula von der Leyen formally relaunched negotiations in June 2022. The breakthrough came during Europe’s College of Commissioners visit to New Delhi in February 2025, when both sides committed to concluding by year-end. They beat the deadline by five months.

The final push happened under extraordinary pressure. As Trump’s 50% tariffs decimated Indian exports to the US, textiles, gems, jewellery, shrimp, and leather saw exports plunge catastrophically, India needed alternative markets urgently. The EU, facing its own trade tensions with Washington and trying to reduce China dependence, needed a manufacturing partner that shared democratic values.

The result? A deal neither side could afford to walk away from.

2. The Anatomy of a $27 Trillion Bargain

Let’s cut through the diplomatic language and examine what has been announced so far.

Note: Final FTA text remains subject to legal scrubbing and ratification by all 27 EU member states plus the European Parliament.

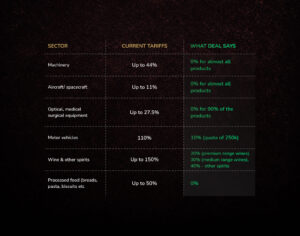

For India: Immediate Relief, Long-Term Gain

According to official announcements, the EU has agreed to eliminate tariffs on 99.5% of Indian goods exports, with nearly 90% moving to zero duty as soon as the FTA comes into force. This is not a slow or phased reduction. It is a sharp, one-shot removal of tariffs.

The immediate beneficiaries? Labour-intensive sectors that employ millions:

These sectors alone represent approximately $33 billion in annual exports and are the backbone of India’s MSME ecosystem. The deal would transform their economics overnight. Indian textile exporters, who currently compete against Bangladesh’s zero-duty access to the EU’s $263.5 billion market, would stand on equal footing.

Commerce Minister Piyush Goyal has projected that India’s textile exports to the EU could jump from $7 billion annually to $30-40 billion, potentially creating 6-7 million new jobs.

For the EU: Access to Tomorrow’s Growth Engine

The EU didn’t exactly extract concessions, it made a calculated bet on India’s consumption story.

India has reportedly agreed to eliminate or reduce tariffs on 96.6% of EU goods exports over 10 years. But the structure matters more than the headline number. India’s tariff reductions are phased and strategic: 30% of trade value reportedly goes to zero immediately, 93% eventually reaches zero over time, and sensitive sectors get quota-based access or longer phase-ins.

The deal’s architecture reveals what India considers non-negotiable. Dairy, cereals, poultry, soymeal, and select fruits reportedly remain heavily protected or excluded entirely, politically sensitive sectors employing millions ahead of state elections.

3. The $75 Billion Opportunity: Sectors on Steroids

The numbers suggest targeted growth, not broad-based liberalization.

Textiles: From $7B to $40B- The Bangladesh Factor-

India’s textile and apparel industry, already the country’s second-largest employer after agriculture with 40 million workers, faces a transformational moment. But to understand the stakes, you must understand the Bangladesh problem.

Bangladesh, exploiting its Least Developed Country status, captured 21.4% of the EU’s $96 billion apparel market, $30 billion annually, with zero-duty access. India, facing 11-12% tariffs since losing EU GSP+ benefits in 2014, was stuck at 4.9% market share ($7 billion). Between 2018-2024, India’s market share declined 92 basis points while Bangladesh gained. In home textiles, Pakistan displaced India: 13.2% market share versus India’s 6.7%.

The competitive handicap was existential. Indian exporters have been competing with one hand tied behind their backs for over a decade. The FTA would eliminate this structural disadvantage overnight.

Zero-duty access would put India on competitive parity with Bangladesh for the first time since 2001. Industry body CITI projects India can hit $100 billion in textile exports by 2030, with the EU accounting for $30-40 billion, potentially creating 6-7 million new jobs.

Critical timing detail: Bangladesh graduates from LDC status in 2026 but gets a three-year grace period until 2029, maintaining zero-duty access. The FTA would give India a three-year window to capture market share before Bangladesh loses its advantage.

Gems, Marine Products & Services-

Gems & Jewellery: The 2-4% tariff elimination might sound minor, but margins in this sector are razor-thin. India’s exports to the EU stood at $2.7 billion in 2024, competing against China and Thailand’s zero-tariff advantage. The Gem & Jewellery Export Promotion Council projects bilateral trade could double to $10 billion within three years. This comes as US tariffs decimated India’s gem exports to America, which crashed 44% in 2025.

Marine Products: India’s shrimp exporters faced crisis in 2025 when US tariffs reached 58-60% (including anti-dumping duties). Farm-gate prices crashed 19-40% in August alone. The sector pivoted hard, Vietnam saw 100% growth in Indian seafood imports, Belgium recorded 90% growth. The EU FTA would institutionalize that pivot with zero-duty access. The Marine Products Export Development Authority estimates this could add $2-3 billion annually.

Services: Lost in goods-trade headlines is a services revolution. The EU has reportedly committed to opening 144 services sub-sectors to India versus 102 India offered to EU, potentially India’s most ambitious services liberalization in any FTA. For India’s IT, professional services, and education sectors, this creates access to a €26 billion annual market (2024 figures). The mobility framework would allow temporary entry for Indian professionals in 37 sub-sectors. This isn’t about call centres, it’s about Indian consulting firms and edtech platforms competing on equal terms in European markets.

4. The US Tariff Cushion: Myth vs. Reality

Can the EU FTA genuinely offset the catastrophic impact of 50% US tariffs? The honest answer: partially, not fully.

The math: India’s exports to the US totaled $86.5 billion in FY 2024-25. Exports to the EU: $75.85 billion. The markets are roughly equal in size, but the sectors differ significantly.

Overlapping sectors (textiles, gems, leather, marine products) would get immediate relief. These account for roughly $33-35 billion of US-bound exports that faced 50-70% demand collapse. Redirecting even half that volume to the EU, with zero-duty access, could save hundreds of thousands of jobs.

Non-overlapping sectors face harsher reality. Auto components ($2.2 billion to US), engineering goods ($16 billion across all markets), and certain chemicals don’t have perfect EU substitutes. These exporters must absorb losses, find third markets, or cut margins.

But the strategic imperative runs deeper than trade diversion. The FTA would help address India’s $99.2 billion trade deficit with China (FY 2024-25), where dependence on electronics, solar panels (70% of India’s solar capacity relies on Chinese equipment), and pharmaceutical APIs creates strategic vulnerabilities. The deal’s machinery and chemical provisions offer India pathways to diversify high-tech imports from democratic Europe rather than authoritarian Beijing.

Three strategic objectives achieved:

First, immediate breathing room for labour-intensive sectors hemorrhaging orders. Textile exporters in Tirupur, shrimp processors in Andhra Pradesh, leather manufacturers in Kanpur get alternative growth paths.

Second, accelerated diversification already underway. India’s export reliance on the US (20% of total exports) was always a vulnerability. The FTA would lock in the EU as a reliable, rules-based alternative representing 12% of exports with room to grow to 18-20%.

Third, a market signal about India’s attractiveness as a manufacturing hub despite US tariff chaos. When global brands see India securing zero-duty access to the world’s richest consumer market, it influences supply chain decisions.

5. The Execution Trap: Turning Signatures into Success

Free trade agreements die not in negotiations but in implementation. The India-EU FTA faces execution challenges that will determine whether it’s transformative or merely transactional.

Challenge 1: The Ratification Marathon

Here’s the timeline reality: The FTA must undergo legal scrubbing and translation (6-12 months), then ratification by all 27 EU member states plus the European Parliament (6-12 months). Any single state can derail it. France has already raised concerns about agricultural imports. Italy worries about textile competition.

Earliest implementation: Q4 2026 or Q1 2027.

Meanwhile, Indian exporters face competitive pressure right now. Without preferential access since losing GSP+ in 2014, they’ve been competing at a 11-12% tariff disadvantage against Bangladesh for over a decade. Orders continue flowing to Dhaka daily. The question isn’t whether the FTA helps, it’s whether exporters can maintain market position through the 12-18 month ratification period.

Challenge 2: CBAM and Climate Compliance

The EU’s Carbon Border Adjustment Mechanism (CBAM) isn’t part of the FTA, it’s a horizontal regulation applying to all partners. Currently covering six products including steel and aluminium, CBAM is designed to expand to all industrial goods, potentially eroding tariff benefits through back-door carbon costs.

India’s steel exporters, currently shipping 1.6 million tonnes to the EU annually, could face carbon levies of 10-15% unless industries upgrade to meet EU emission standards. India’s steel industry carbon intensity is 30% higher than the EU average, requiring an estimated $50-100 billion capital investment in green steel over 10 years.

The FTA reportedly includes technical dialogue mechanisms to address CBAM, with commitments to accredit Indian carbon verifiers and recognize India’s domestic carbon markets. But the ultimate solution requires India’s industrial base to decarbonize, a decade-long transformation, not a policy adjustment.

Challenge 3: The Quality and Standards Gap

Zero-duty access becomes meaningless if products can’t meet EU standards. European technical, environmental, and product norms are among the world’s strictest. Indian exporters, particularly MSMEs, face higher costs for testing, certification, cleaner technologies, and documentation.

The textile industry might capture $30 billion in EU exports, but only if Indian mills can meet REACH chemical regulations, achieve carbon neutrality targets, and document supply chain traceability under the EU Deforestation Regulation (EUDR).

The Federation of Indian Export Organisations (FIEO) estimates 15-20% of potential exporters will struggle with compliance costs in the first three years. The FTA reportedly includes capacity-building provisions and SME contact points, but whether that’s sufficient remains to be seen.

Conclusion: A Deal Forged in Crisis, Built for Decades

The India-EU FTA isn’t the product of idealistic globalization. It’s the offspring of geopolitical necessity, born when the US weaponized trade, China became simultaneously too risky and too dominant in supply chains, and both sides faced urgent economic pressures.

What makes it potentially consequential isn’t just the $27 trillion combined market or the 2 billion people it would cover. It’s the strategic paradigm shift it represents.

For two decades, India’s trade policy prioritized strategic autonomy over deep integration. It signed FTAs cautiously, protected sensitive sectors aggressively, and kept one foot outside globalization’s door. This FTA, if ratified and implemented as announced, would mark a departure: a bet that Indian manufacturing can compete not just on cost but on quality, that its services can dominate globally, and that economic integration with like-minded democracies serves national interest.

For the EU, this represents diversification in an age of weaponized interdependence. The bloc cannot afford dependence on China for manufacturing or exclusive reliance on unpredictable US security guarantees. India, whatever its complexities, shares democratic governance, respects rules-based systems, and offers scale.

The execution challenge is real: ratification uncertainty, CBAM compliance, quality standards, and political headwinds create genuine obstacles. But the alternative, India facing US tariff walls without alternative markets, Europe remaining exposed to Chinese supply chains, is worse for both sides.

In January 2026, this wasn’t theoretical. Indian textile exporters were rebooking orders previously lost to Bangladesh. European automakers were finalizing investment decisions for Indian manufacturing plants to serve 1.4 billion consumers.

The mother of all deals isn’t just about what was signed in New Delhi. It’s about what happens in Tirupur, Stuttgart, Surat, and Brussels over the next decade.

That story, pending ratification, is just beginning.

Disclamer

This article is for informational purposes only. All data and statistics are sourced from official government releases, European Commission documents, industry reports, and media coverage as of January 2026. While efforts have been made to ensure accuracy, trade policy remains subject to implementation timelines, regulatory changes, and political developments. Readers should consult trade experts and legal advisors before making business decisions based on FTA provisions. References to specific sectors, companies, or regions are illustrative and not recommendations.