July 2025’s Amazon Prime Day sealed it: 70% of new Prime memberships flooded in from these rising hubs, eclipsing Mumbai, Delhi, and Bengaluru.

For decades, the prosperity playbook screamed “metro or bust.” Mumbai for money, Bengaluru for bytes, Delhi for deals.

That script? Shredded.

India’s entrepreneurial geography has undergone a profound transformation. The data on new company incorporations, businesses being registered each year reveals the tilt.

Tier-1 cities ride global waves. In 2021, registrations jumped 16%. When funding froze in 2023, they crashed 14%. Then 2024 roared back with a 26% surge.

Tier-2 cities? They move faster, fall softer. 2021 saw a blistering 35% jump in new companies, more than double the metro rate. When 2023’s slowdown hit, Tier-2 cities dipped just 12% versus metros’ 14% plunge. By 2024, they matched the comeback with 26% growth.

The pattern is unmistakable: Tier-2 cities accelerate harder in good times, cushion better in bad times, and recover just as fiercely. The momentum has shifted.

The question isn’t whether this transformation is real.

The question is: How are India’s rising cities reshaping the country’s wealth map, and what does this mean for investors, policymakers, and brands?

This month, we explore India’s Emerging Wealth Corridors.

We cover:

1. Consumption shifts redefining aspirational demand

2. Digital infrastructure powering Tier 2 financial inclusion

3. Real estate and luxury segments finding new traction

4. Employment decentralization and the rise of regional hubs

5. What this means for long-term wealth creation strategies

1. The Consumption Revolution: Where India Really Shops

There’s a common myth in Indian business that spending in Tier 2 and Tier 3 cities relies mostly on discounts and sales promotions. However, fresh 2025 transaction data from Mintoak, which studied 4 million small and medium merchants across India, completely debunks this idea.

In October 2025 alone, Tier 3 cities showed a strong 51% surge in the total value of digital payments, paired with a 49% increase in the number of transactions. These nearly matching growth rates reveal a “volume-led” trend: more people visiting stores (higher footfall) and making purchases more frequently, all at regular, everyday prices. It’s not about bigger baskets from discounts inflating each transaction, average spend per purchase barely budged. This points to real, growing demand from everyday consumers in smaller cities.

This trend gets even clearer when you look at specific shopping categories in Tier 3 cities (October 2025 vs. October 2024 YoY). Grocery and supermarket payments grew 51–59%, pharmacies and health retail rose 43%, quick-service restaurants (QSRs) and cafés jumped 38% in transaction volumes, electronics and mobiles increased 46%, and fashion/apparel transactions climbed 41%.

Even aspirational categories (not tied to seasons or sales) showed the same strength: watches and jewelry up 66–77%, consumer durables rose 44%, and home/lifestyle retail grew 37%. When both everyday essentials and luxury-ish buys grow steadily by 40–60% at the same time, it proves broad, year-round demand. This comes from rising incomes, more digital payments, and real purchasing power in India’s emerging middle class in Tier 2/3 cities. The old story that these markets only spend when prices drop is officially busted.

2. The Infra Buildout Turning Tier 2/3 India Into a Consumption Powerhouse.

None of this consumption growth would be sustainable without the digital and physical infrastructure that’s been built over the past five years. In July 2025 alone, UPI processed 1,947 crore transactions worth rupees 25.1 lakh crore, that’s a 35% year-on-year increase in volume and 22% in value. But the geographic distribution is what matters most: Tier 2/3 account for 72% of BHIM UPI transactions (2025 data) and 80% new registrations, with Tier 3 MoM surges. As the IMF noted, “UPI’s success is a story of digital acceleration unlocked by interoperability,” and when 60% of new online sellers since 2021 come from Tier 2 or smaller cities, that’s proof the infrastructure for commerce is genuinely in place.

The physical infrastructure story is equally impressive. Government spending on infrastructure jumped from rupees 5 lakh crore in 2021-22 to rupees 11.11 lakh crore in 2024-25. The UDAN scheme connected 88 cities and operationalized 618 routes, with plans for 120 new destinations. Smart City initiatives have pumped rupees 1.47 lakh crore into connectivity. India now has over 500 million smartphone users, with the fastest growth coming from smaller cities, enabling everything from telemedicine to vernacular e-commerce to function seamlessly. This isn’t aspirational infrastructure that might enable growth someday, it’s operational infrastructure enabling growth right now.

3. Real Estate and Luxury Segments Finding New Traction

Tier 2 and Tier 3 cities in India are emerging as the new powerhouses of residential real estate, delivering impressive growth, affordability, and investor-friendly metrics that outshine many metro markets.

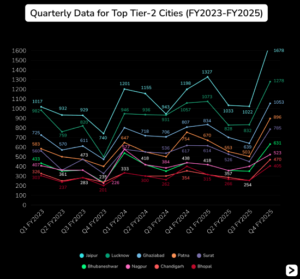

Residential sales values in India’s top 15 Tier 2 cities grew 6% year-on-year to rupees 40,443 crore in Q1 2025, even as unit sales dipped 8% to 43,781 homes, reflecting a shift toward higher-value properties amid strong demand. Rental yields here consistently range from 4.5-5.5%, well above Mumbai’s subdued 2-3% and the national average of around 4%, making these markets attractive for steady income streams. Property prices remain up to 30% lower than in Tier 1 metros, yet appreciation rates often hit 15-25% annually, creating compelling entry points for first-time buyers and investors priced out of pricier urban centers.

City-level standouts underscore this momentum. Lucknow led with a remarkable 48% surge in housing sales value in Q1 2025, driven by infrastructure upgrades and job growth. In affordable hubs like Coimbatore and Mysore, entry-level homes start at rupees 3,000-6,000 per sq ft, roughly one-third the cost of comparable metro properties, drawing young professionals and families seeking value without compromise. Surat and Ahmedabad also posted solid gains, with sales volumes and values climbing steadily through H1 2025 as IT parks, highways, and smart city initiatives fuel migration and spending.

Institutional interest is surging too. Tier 2/3 cities captured around 40% of land acquisitions in 2024 (over 3,000 acres across key deals), signaling developer confidence in long-term demand. Housing sales across 60 such cities rose about 23% to roughly 680,000 units last year, per CREDAI trends, while NRIs shifted 25-35% of their investments toward promising spots like Pune and Kochi. Foreign direct investment in real estate ticked higher, with Tier 2 opportunities drawing growing shares from global funds eyeing stable, high-yield plays.

This isn’t a fleeting trend, rising incomes, digital adoption via UPI, and government initiatives like PMAY 2.0 are fueling sustained demand. Tier 2 cities now drive over 40% of home loan volumes (up from 60% market share in 2024), blending urban amenities with 4.5-5.5% yields and 15-25% appreciation, better risk-adjusted returns than metros.

Prosperity used to have a zip code.

In 2025, it became a PIN code-wide phenomenon.

4. Employment Decentralization and the Rise of Regional Hubs

Employment and startup data represent the most compelling evidence of Tier 2 and Tier 3 cities’ unstoppable rise, proving these markets aren’t just catching up, they’re poised to redefine India’s economic future for wealth creators and investors alike.

Startups Have Already Shifted

Over 45% of DPIIT-recognized startups now originate from Tier 2/3 cities and this isn’t nostalgia-driven, the economics are unbeatable. Office rents in Indore run 60% lower than Bengaluru, while skilled software engineers in Bhubaneswar command 30-50% less than Mumbai peers, delivering identical output. Startup India’s impact is massive: 17.6+ lakh jobs created since inception, with Tier 2/3 regions adding thousands monthly through 2025.

Job Creation Is Explosive

Tier 2 cities posted 42% job growth from late 2024 to early 2025, more than double metro gains of 19%, led by manufacturing (+29%) and IT (+17%). Standouts like Lucknow (3,000+ startups in IT/edtech), Jaipur (3,800+ across textiles/tourism), and Coimbatore (1,700+ D2C/tech firms) demonstrate concentrated ecosystems rivaling Tier 1. Bharat-focused startups raised rupees 1.2 billion in H1 2025 alone (+55% YoY), with edtech and SaaS dominating.

Global Capital Is Following

Over 1,500 Global Capability Centers targeted Tier 2 expansion in 2025 (up from 1,200 in 2024), chasing the unbeatable trio of talent + infrastructure + costs.

The conclusion is clear, High-growth companies aren’t “emerging” from Tier 2/3, they’re already there, scaling faster with superior economics.

5. What This Means for Wealth Creation and Capital Allocation

Assets under management from Tier 2 and 3 city investors have climbed steadily over six years, revealing a powerful structural shift. While total mutual fund AUM grew 2.5x from FY18’s rupees 21 trillion to FY24’s rupees 53 trillion, the distribution shows increasing penetration beyond metros. Tier 2/3 cities maintained their 13% share even as the pie expanded dramatically, while Next 20 cities surged from 6% to 9% and Next 75 cities held steady at 4%, together commanding 23% of the rupees 53 trillion AUM by FY24, up from 17% of rupees 21 trillion in FY18. Meanwhile, Top 5 cities’ dominance declined from 63% to 53%, signaling clear wealth democratization.

But 2025 marked a pivotal acceleration, sophisticated clients in these hubs began channeling funds into family office services, hedge fund strategies, and offshore portfolios. Livemint reports that wealthy non-metro investors are snapping up concentrated equity and debt management, fueled by rising awareness and homegrown wealth builders like entrepreneurs and professionals.

Income tax data underscores the velocity: filers earning rupees 50 lakh to rupees 1 crore have quadrupled in these cities, while MSMEs here now claim 51% of India’s total registration, powering real wealth factories on the ground. Spotlight cities tell the story: Coimbatore draws domestic and global R&D giants; Jaipur logged 5,060 new companies in a single year; and Lucknow’s real estate outpaces Delhi’s appreciation. These aren’t outliers, they signal systematic investment flows compounding across decades.

McKinsey forecasts 18 Tier 2 “future arenas” generating $2 trillion in revenues by 2030, up from $690 billion in 2023. Gujarat’s GIFT City and UP’s investor summits locked in $10 billion in 2025 pledges, spanning startups, MSMEs, real estate, manufacturing, IT, and consumer sectors, all firing in unison. This multi-industry, multi-geography momentum, distributed and resilient, ensures tomorrow’s HNWIs emerge from today’s bold bets.

6. The Investment Thesis Going Forward

Let’s be clear about what happened in 2025. Tier 2 cities didn’t “catch up” to metros, they reimagined what Indian prosperity looks like and built business models that work better in their specific contexts. When GCCs surge 21% in smaller cities, when digital payments in Tier 3 grow faster than Mumbai, when Coimbatore property registrations jump 14.42% and Lucknow housing sales spike 48%, these aren’t temporary blips. This is the new normal, driven by fundamentals, better infrastructure, lower costs, genuine purchasing power, and a generation of entrepreneurs who realized they could build better lives without sacrificing everything to live in overpriced, overcrowded metros.

For three decades, success meant proximity to power, how close you were to Nariman Point, Connaught Place, or Koramangala. Now success means proximity to opportunity, and opportunity has decentralized. The ladder to prosperity didn’t break by accident; it broke because millions of Indians realized they didn’t need it anymore. For investors and wealth managers, that shift creates opportunities that haven’t existed in India’s modern economic history, the chance to back businesses, real estate, and wealth creation in markets that offer better unit economics, higher growth rates, and lower entry multiples than their metro equivalents.

That NASSCOM prediction about half of India’s new ventures emerging from Tier 2 and 3 cities by 2035? Based on 2025’s trajectory, it’s conservative. The geography of Indian wealth is being rewritten in real time, and the investors who recognize this early will be the ones capturing the outsized returns over the next decade.